Are distributions required from a complex trust?

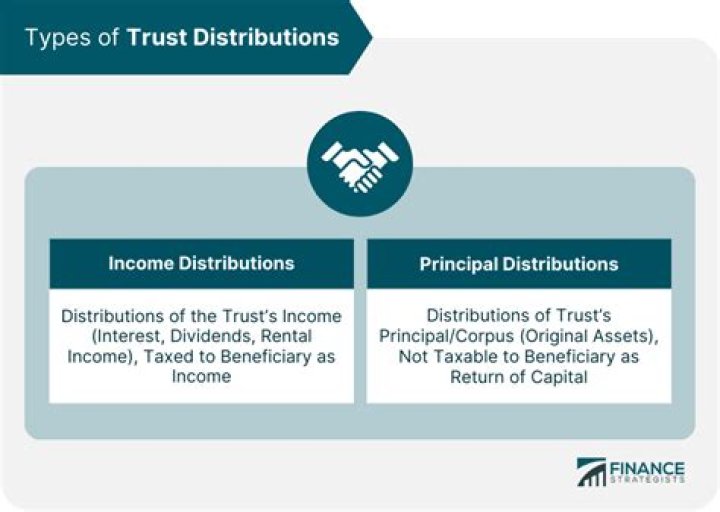

Unlike a simple trust, a complex trust is not required to distribute all its accounting income currently; rather, the accounting income of a complex trust may be accumulated (Sec. 661), distributed to charity (Regs. Sec.

Who pays taxes on a complex trust?

Does a trust file its own income tax return? Yes, if the trust is a simple trust or complex trust, the trustee must file a tax return for the trust (IRS Form 1041) if the trust has any taxable income (gross income less deductions is greater than $0), or gross income of $600 or more.

Can you distribute from one trust to another?

Therefore, when distributing to another trust, it is necessary to ensure that the trust is listed as a beneficiary in the trust deed. Just because both trusts have the same beneficiaries listed in their trust deeds does not mean that the trustees of both trusts may make distributions between the two trusts.

How are complex trusts different from simple trusts?

Unlike a simple trust, a complex trust is not required to distribute all its accounting income currently; rather, the accounting income of a complex trust may be accumulated (Sec. 661), distributed to charity (Regs. Sec. 1.661 (b)- 2 ), or both. A complex trust can also make distributions from corpus (Sec. 661).

How is income allocated in a simple trust?

A Simple Trust must allocate all Ordinary Income to beneficiaries; a Complex Trust frequently does according to the provisions of the trust. Distributions can be allocated by percentage amongst the beneficiaries or alternatively by explicit amounts, as stated in the provisions of the trust document.

Is the distribution deduction limited to trust income?

The distribution deduction is limited to the lesser of trust accounting income required to be distributed and distributable net income (DNI) (Sec. 651 (b)).

How much did a complex trust make in 2018?

I’m helping the trustee of a complex trust with the 2018 Federal Fiduciary Return. In 2018 the trust sold all shares of a fund, resulting in total proceeds of about $70k. The cap gains totaled about $20k. The trust also had $14k in cash prior to the sale.