Are facilitative costs deductible?

Special rules and exceptions apply to certain transaction costs described as “inherently facilitative” (capitalizable) or, alternatively, as nonfacilitative (potentially deductible), such as integration expenses, employee compensation, and amounts eligible under the “bright-line” date rule described in Regs.

What transaction costs are capitalized?

Taxpayers typically incur significant transaction costs when undergoing a transaction involving a restructuring, acquisition, disposition, sale of assets, or sale of stock. The default rule under section 263 is that all transaction costs that facilitate a transaction must be capitalized.

Should transaction costs be capitalized?

Generally, costs that facilitate a transaction must be capitalized. These costs include amounts paid in the process of investigating or otherwise pursuing the transaction.

Should you capitalize or deduct the transaction costs of a failed deal?

Generally, if the capital transaction is abandoned after the expenses were incurred, the accumulated expenses may be deducted, under the authority of Sec. 165, as a loss. These capital expenditures, however, were an intangible asset that would have offset the proceeds of sale (had the offering succeeded).

Can you amortize transaction expenses?

BOOK TREATMENT: Transaction costs are not considered part of the fair value exchanged between the buyer and seller and are therefore expensed as incurred. These capitalized costs are added to the tax basis of the assets and typically amortized of the life of the underlying asset(s).

Can professional fees be Capitalised?

Legal and professional fees incurred in connection with changes in how the ownership of a business is structured are generally regarded as capital for tax purposes and not allowable as a revenue deduction.

Are consulting fees capitalized or expensed?

The types of costs capitalized during the application development phase include employee compensation, as well as consulting fees for third-party developers working on these projects. Costs related to the preliminary project stage and post-implementation activities are expensed as incurred.

Are acquisition costs amortized or depreciated?

It is important to note that in an asset acquisition (as opposed to a stock transaction) these costs are allocated to the assets purchased, and can be depreciated or amortized over the life of the assets acquired.

When should professional fees be capitalized?

Projects such as building construction included in the fixed asset value of the building, the cost of professional fees (architect and engineering), permits and other expenditures necessary to place the asset in its intended location and condition for use should be capitalized.

Are acquisition costs capitalized or expensed GAAP?

Acquisition-related costs or transaction costs Acquisition-related costs are expensed as incurred, except for costs of issuing debt and equity securities, which are accounted for under other GAAP.

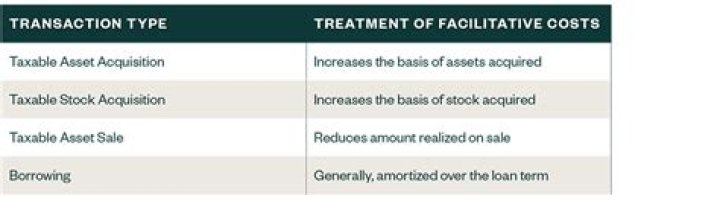

How are facilitative costs treated by the IRS?

Facilitative costs. A taxpayer must capitalize a cost that facilitates a transaction described in Reg. § 1.263 (a)-5 (a). Whether a cost facilitates such a transaction is based on all the facts and circumstances. The cost must be paid to investigate or otherwise pursue the transaction.

How are capitalized costs treated by the IRS?

Costs that are facilitative and must be capitalized under Reg. § 1.263(a)-5 may be recoverable immediately, may be recoverable over time, or may never be recoverable. The structure of the transaction and the taxpayer’s role in the transaction (e.g., acquirer or target) determine how the capitalized costs are treated.

What is the definition of inherently facilitative cost?

An “inherently facilitative” cost is an amount paid for certain types of activities (i.e., services performed) to investigate or otherwise pursue the transaction. Inherently facilitative costs must be capitalized regardless of when the related services are performed.

How are facilitative costs included in an acquisition?

Facilitative Costs. A taxable acquisition by the taxpayer of a target’s assets that constitute a trade or business; and A taxable acquisition of a significant ownership interest in a business entity (whether the taxpayer is the acquirer in the acquisition or the target of the acquisition).