Are safe harbor contribution mandatory?

A Safe Harbor Match is a form of mandatory employer contribution. There are three types of mandatory employer contributions, two of which are technically matches: Non-Elective Safe Harbor: Eligible employees get an annual employer contribution of 3% of their salary.

Does a safe harbor plan have to match catch up contributions?

Requirements of a Safe Harbor Feature. If you are thinking there must be a catch, you are correct. In non-safe harbor plans, employer contributions are discretionary; the employer decides what matching or nonelective contribution, if any, to make in a particular year.

Can a safe harbor plan be top heavy?

According to the IRS, “A plan is top-heavy when the owners and most highly paid employees (‘key employees’) own more than 60% of the value of the plan assets.” A safe harbor 401(k) that has only elective deferrals and safe harbor matching contributions is generally exempt from being top-heavy.

Can I stop my safe harbor match mid-year?

Allows an employer to make a mid-year amendment to a safe harbor plan to reduce or suspend safe harbor contributions to non-highly compensated employees (“NHCEs”) regardless of whether the employer is suffering an economic loss or has provided a notice that that the employer may suspend or reduce the safe harbor …

What are the requirements for a safe harbor contribution?

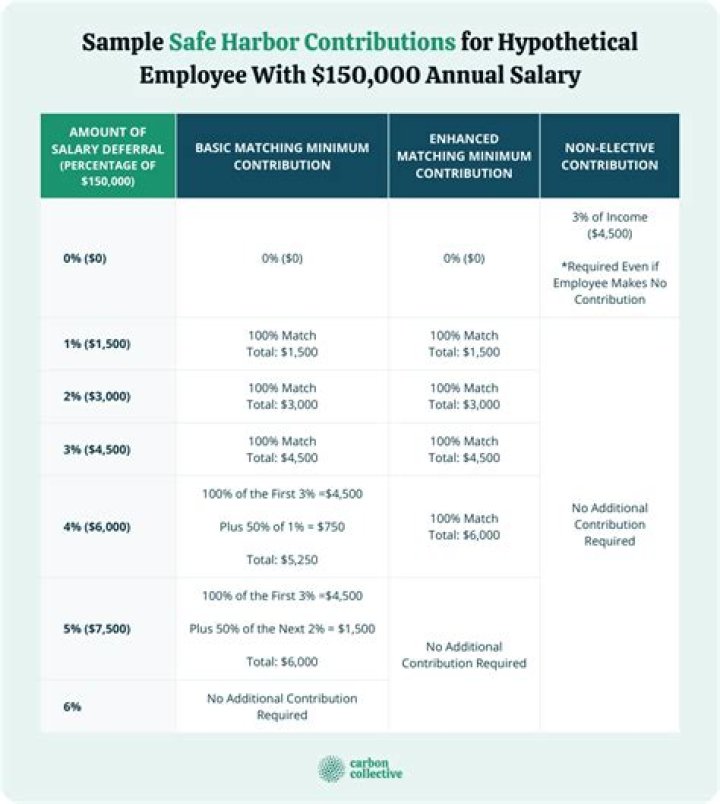

When the basic safe harbor match is used, a plan must provide a matching contribution at a minimum rate of dollar for dollar on the employee deferrals up to 3% of pay and 50¢ per dollar on the next 2% of pay.

Can a company contribute to a safe harbor 401k plan?

You can design your safe harbor plan to limit matching contributions to only those employees who defer compensation, or you can make contributions for everyone, including those who don’t contribute to their own plans. 6 Plans can allocate contributions in one of three ways:

Can a company withdraw from a safe harbor plan?

Finally, the plan may not allow for distributions of the employer’s safe harbor contributions during employment, even for hardship, although employee deferral contributions can be withdrawn for hardship if the plan so provides. Annual notices for all plans must be given within a reasonable time.

Can a business owner match a safe harbor plan?

The amount you match will depend on your own contributions as a business owner. A long vesting schedule is not allowed with safe harbor plans, contributions are fully vested when made. This means you have to give all employees their share — even those who leave or are fired during the year.