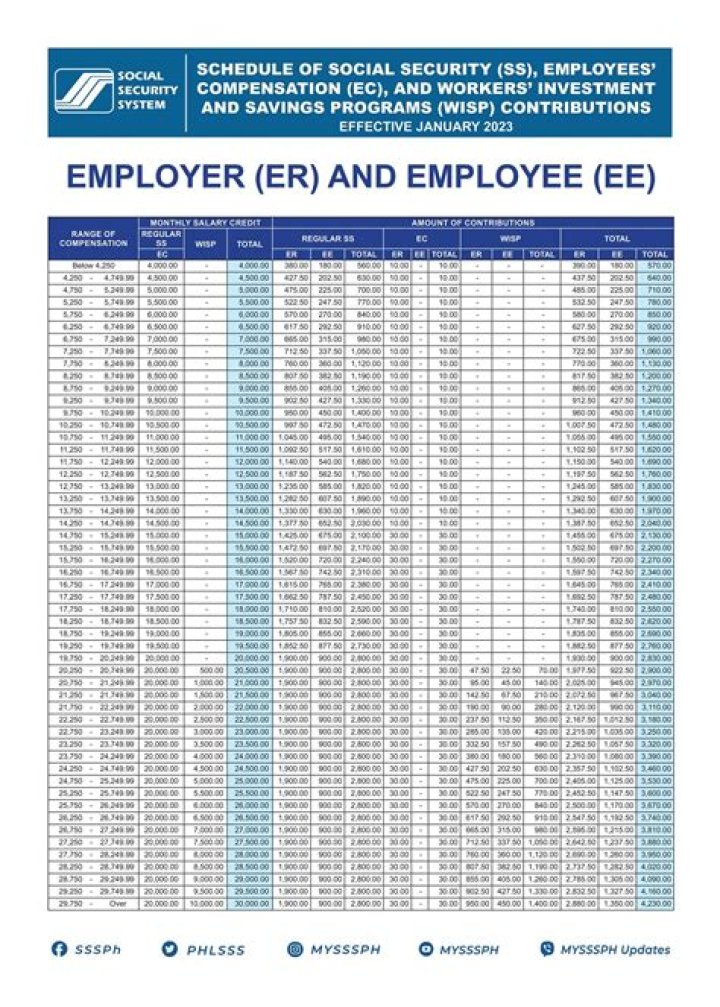

Are SEP contributions employee or employer?

Can I make catch-up contributions to my SEP? No, SEPs are funded by employer contributions only. Catch-up contributions apply only to employee elective deferrals. However, if you are permitted to make traditional IRA contributions to your SEP-IRA account, you may be able to make catch-up IRA contributions.

Are all SEP contributions employer?

SEP plan limits SEP plans (that are not SARSEPs) only allow employer contributions. For a self-employed individual, contributions are limited to 25% of your net earnings from self-employment (not including contributions for yourself), up to $58,000 (for 2021; $57,000 for 2020).

How many employees SEP IRA?

Because the employer must make proportional contributions, SEP IRAs are generally best for very small businesses with less than 10 employees. Furthermore, seasonal businesses can also benefit from SEP IRAs because contributions are discretionary.

What is another name for a SEP IRA?

A SEP IRA and an individual 401(k), also known as a solo 401(k), are both retirement accounts that allow employer contributions.

With a SEP IRA, only the employer contributes. Employers must contribute the lesser option of the two. The first option—25 percent of compensation—is also the limit for how much you can contribute to each eligible employee.

Can a SEP IRA be established by an employee?

A SEP IRA plan can be established by a business owner with employees. A SEP IRA is funded 100% by the employer, employees do not contribute.

Are there any disadvantages to a SEP IRA?

SEP Disadvantages Employees are 100% vested in employer contributions once they are made. No vesting schedule may be attached to SEP contributions. You must make the same percentage contribution for all eligible employees.

What’s the maximum contribution to a SEP IRA?

The 2020 SEP IRA contribution limit is $57,000 and the 2019 SEP IRA contribution limit is $56,000. Contributions to a SEP IRA are generally 100% tax deductible and investment earnings in a SEP IRA grow taxed deferred.

Can a SEP IRA be used for a side gig?

This is an advantage for the employer as the employer is not responsible for the underlying investments. SEPs are great for people who have a side gig because it allows the worker to fully contribute to their employer’s 401 (k) plan and use a SEP IRA for self-employment income.