Can a CPA be a 1031 intermediary?

However, CPAs, attorneys, investment bankers, and real estate agents/brokers fall under the ‘agent’ category, so they cannot act as your Qualified Intermediary. To break it down, the exception allows agents to act as intermediaries only if they are working on a specific property type in the 1031 exchange.

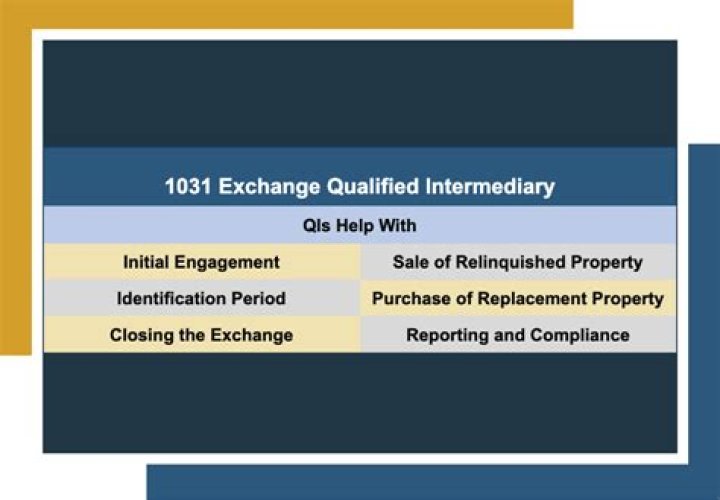

Who can help me with a 1031 exchange?

The Five Professionals to Have on Your 1031 Dream Team

- 1031 Qualified Intermediary. This is your point guard and your key position.

- An agent/broker who understands 1031 Exchanges. This is your guard.

- An experienced attorney.

- A CPA.

- A closing agent.

Can I be my own qualified intermediary?

There aren’t any licensing or educational requirements necessary to be a qualified intermediary. To be considered qualified under Internal Revenue Code (IRC) section 1031, you cannot be an intermediary for yourself, nor can anyone related to you or anyone who has acted as your agent in the previous two years.

Do you have to have a qualified intermediary for a 1031 exchange?

A 1031 exchange allows you to avoid capital gains tax by immediately reinvesting money from an asset sale into another “like-kind” asset purchase. You will need a qualified intermediary to complete this exchange.

Do I have to use a qualified intermediary for a 1031 exchange?

The odds of that you will find someone who wants to swap properties are slim. Probably the most important rule is that taxpayers must hire a 1031 intermediary prior to transferring their old property.

However, CPAs, attorneys, investment bankers, and real estate agents/brokers fall under the ‘agent’ category, so they cannot act as your Qualified Intermediary. Additionally, any business or individual who is affiliated with the agent also cannot act as a Qualified Intermediary.

Can an attorney be a qualified intermediary?

In some jurisdictions, an attorney can be designated as your Qualified Intermediary, but it can’t be your regular legal counsel — IRS rules state that legal counsel can only act as a Qualified Intermediary if he or she has not performed services for the client in the prior two years unless the work is related to a …

What do you need to know about the 1031 exchange?

A 1031 exchange — also recognized by the IRS as a like-kind exchange — enables real estate investors to defer the capital gains tax liability on the sale of an investment property by using those proceeds to buy another property.

Can a like kind exchange be tax deferred?

Gain deferred in a like-kind exchange under IRC Section 1031 is tax-deferred, but it is not tax-free. The exchange can include like-kind property exclusively or it can include like-kind property along with cash, liabilities and property that are not like-kind.

Can a loss be recognized under Section 1031?

You can’t recognize a loss. Under the Tax Cuts and Jobs Act, Section 1031 now applies only to exchanges of real property and not to exchanges of personal or intangible property. An exchange of real property held primarily for sale still does not qualify as a like-kind exchange.

How does SEC 1031 apply to real property?

As a practical matter, taxpayers could often offset relinquished personal property with replacement personal property to defer most or all of the gain on the exchange. Following the TCJA, Sec. 1031 only applies to real property.