Can a grantor trust make loans?

Assets owned by an irrevocable trust are intended to be estate tax-free (and usually generation skipping transfer tax-free, too). Loans and sales transactions between the grantor and a grantor trust are normally income tax-free.

Is a loan from a trust taxable?

You’re taxable on the lower of the capital sum and the trustees’ available income in the tax year in which the capital sum is paid to you (or to your spouse or civil partner). If you were taxable on the original loan, it’s only the excess of the additional loan over the original loan that’s treated as a capital sum.

Can a trust make an interest free loan to a beneficiary?

A trust can loan money to a beneficiary if this is allowed by the trust documents. A trust loan lender can provide a loan to the trust with a note and deed of trust recorded against real estate owned by the trust.

Can an irrevocable trust make a loan to the grantor?

An irrevocable trust can obtain a loan using real estate assets as collateral. The irrevocable trust loan would need to be approved by the successor trustee. The successor trustee will also need to review and sign various loan documents and disclosures.

Are gifts to grantor trusts taxable?

Any transfer to the grantor trust will be subject to gift taxes unless consideration of equal value is received by the grantor in return. The funding of a grantor trust with the initial gift typically will be a taxable gift, but most often sheltered by the lifetime exclusion amount.

What happens to a loan trust on death?

On the death of the settlor, any outstanding loan from a loan trust will be an asset of the settlor’s estate and therefore potentially subject to inheritance tax.

Can you top up a loan trust?

A Loan Trust normally has to be set up with new monies – you cannot normally use an existing bond to create a Loan Trust. The settlor lends monies to the trustees who in turn buy the bond. You can generally top up an existing Loan Trust and the settlor can do this by either way of a further loan or by way of a gift.

Does trust interest in possession?

An interest in possession trust is a trust in which at least one beneficiary has the right to receive the income generated by the trust (if trust funds are invested) or the right to enjoy the trust assets for the present time in another way. Such a beneficiary is also known as an income beneficiary or life tenant.

How does a loan trust work?

Using a Loan Trust allows clients access to their original capital at any point and in any amount but the growth will not be included in their estate for IHT purposes. With a Loan Trust, the loan can be waived in part or in full at any time. Insurance companies can offer a “Deed to waive a loan”.

How does a loan plan work?

The Loan Plan is easy to set up and to operate. The client doesn’t give up access to cash – it is merely loaned to the Plan. The client establishes a trust, appoints trustees and may nominate beneficiaries. The client makes a loan to the trustees who use the Loan to purchase a Standard Life Bond.

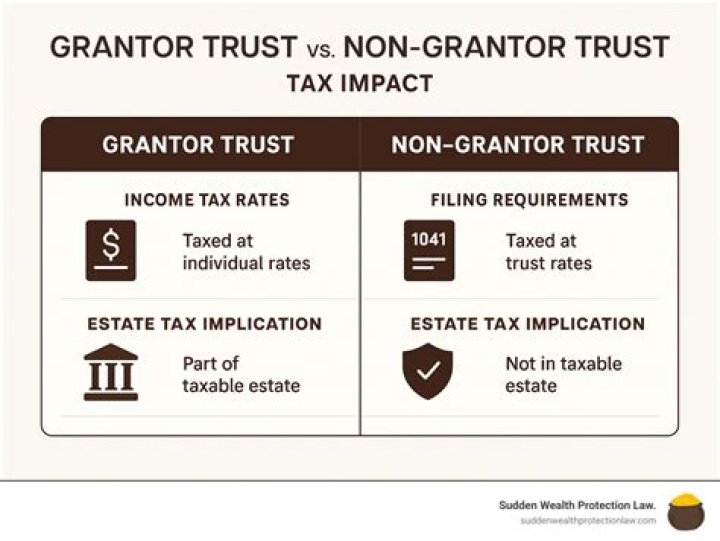

How are grantor trusts taxed?

A grantor trust, such as revocable trust, is taxed directly to the grantor and the grantor reports the income of the trust on his or her own Form 1040. The trustee of the trust has the trust file its own tax return, Form 1041. On that return goes all the trust’s items of income and expense.

Are distributions from a grantor trust taxable?

Grantor trusts, in which all income is taxed to the grantor, regardless of whether the grantor receives distributions from the trust. These trusts are treated as “alter egos” of the grantor for income tax purposes. Trusts that are treated as separate tax entities.

Is interest forgiven taxable?

In general, if you have cancellation of debt income because your debt is canceled, forgiven, or discharged for less than the amount you must pay, the amount of the canceled debt is taxable and you must report the canceled debt on your tax return for the year the cancellation occurs.

Are there income tax implications for a grantor trust?

The trust that you established for estate planning purposes may have some interesting income tax considerations. Be aware of who pays the income tax on the trust income, the opportunities with grantor trust planning, and the income tax effect and distribution planning opportunities for non-grantor trusts.

Do you have to pay income tax on loan to trust?

You can also loan money to the trust, and although the trust must pay you at least a minimum IRS-prescribed interest rate (called the applicable federal rate [AFR]), the interest income is not taxable to you. In addition, your trust’s income tax, paid by you as the grantor, is not considered an additional gift to the trust.

When to use an idgt in a grantor trust?

It is effectively a grantor trust with a purposeful flaw that ensures the individual continues to pay income taxes. IDGTs are most often utilized when the trust beneficiaries are children or grandchildren where the grantor has paid income tax on the growth of assets that they will inherit.

Who is the owner of the assets in a grantor trust?

Under these rules, the individual who creates a grantor trust is recognized as the owner of assets and property held within the trust for income and estate tax purposes. The grantor trust rules allow grantors to control the assets and investments in a trust.