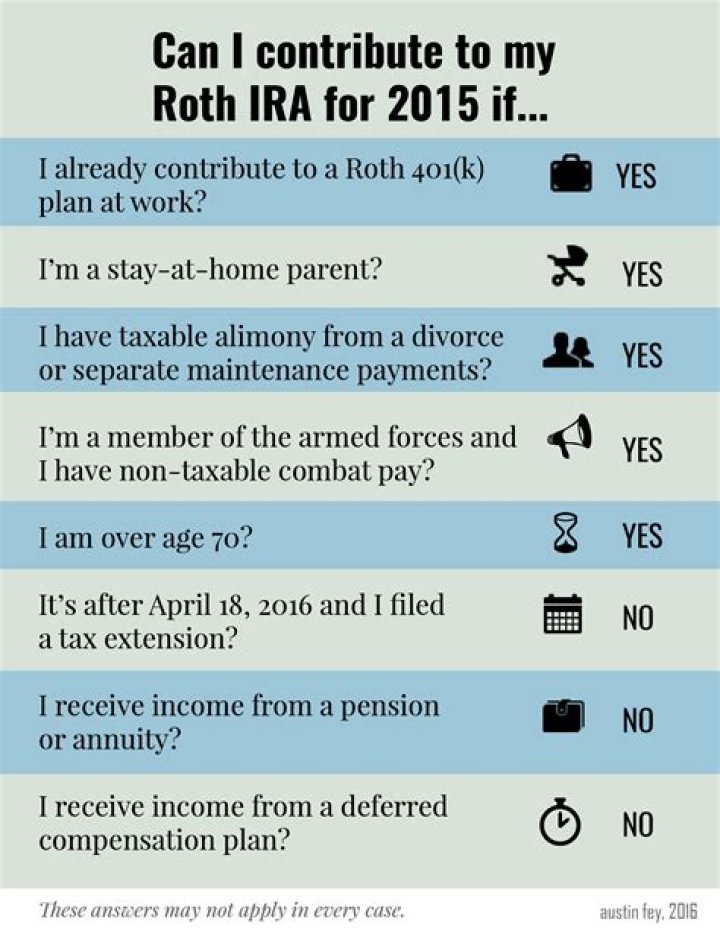

Can a husband contribute to his wife Roth IRA?

You need to have “earned income” (taxable compensation) to contribute to a traditional or Roth IRA. An exception to this rule is a spousal IRA, which allows someone with earned income to contribute on behalf of a spouse who doesn’t work for pay.

How much can married couple contribute to traditional IRA?

Rules on IRA contribution limits You and your spouse can each contribute annually up to $6,000 (for 2019) or 100% of your earned income, whichever is less, into an IRA. In 2019, married couples filing jointly can generally contribute a total of $11,000 ($5,500 per spouse) even if only one spouse had income.

Can a working spouse contribute to a traditional IRA?

If the working spouse is covered by an employer-sponsored plan, their ability to deduct any, some, or all of their traditional IRA contributions will depend on their modified adjusted gross income and tax filing status. These rules are explained in IRS Publication 590-A, which is updated annually.

Are there income limits for a spouse to contribute to a Roth IRA?

There is no income cap for traditional IRA contributions. However, if you want to contribute to a Roth IRA for your spouse (or yourself), there are income limits. For 2020, a married couple filing jointly with a modified adjusted gross income (MAGI) of up to $196,000 is eligible to contribute the full amount to each of their Roth IRAs.

When to deduct contributions to a spousal IRA?

Just like with other traditional IRAs, a couple can deduct the full contribution to a traditional spousal IRA from federal income taxes in tax years 2020 and 2021 if neither is covered by a defined-contribution plan, such as a 401 (k) or an IRA, or a defined-benefit plan, such as a pension plan that’s provided by an employer. 4

Can a spouse contribute to a spousal retirement account?

Making spousal individual retirement account (IRA) contributions is an important way to build up your family’s retirement nest egg if only one spouse is employed. People without paid jobs generally aren’t eligible to contribute to tax-advantaged retirement accounts, such as IRAs, because they don’t have earned income to fund them.