Can an LLC buy a whole life insurance policy?

Under this approach, the business owners would still execute a cross-purchase agreement, but would form an LLC to own a life insurance policy on the life of each owner. However, by using an LLC to own the buy-sell insurance, the LLC owns all the policies, so only one policy per shareholder is needed.

Can an employer buy life insurance on an employee?

Federal law now requires employers to obtain an employee’s permission before purchasing a life insurance policy. By meeting this and other requirements, employers may purchase insurance on their employees and collect upon their deaths.

What does employer paid life insurance mean?

Many employers offer a certain amount of group term life insurance as part of their employee benefits package. If you have this benefit, then your employer may pay for some or all of the premium costs. However, getting all of your life insurance where you work can put your family at risk if something happens to you.

What is considered to be the beginning of an insurance contract?

In general, an insurance contract must meet four conditions in order to be legally valid: it must be for a legal purpose; the parties must have a legal capacity to contract; there must be evidence of a meeting of minds between the insurer and the insured; and there must be a payment or consideration.

What does 1x annual salary mean?

AT A GLANCE: • A cash benefit of 1 times your base annual salary to your loved ones in the event of your death, plus an additional 1 times salary cash benefit if you die in an accident.

Can a business own a life insurance policy?

A life insurance policy can be used for business owners that require cash to begin a business or buy a company. Typically, when you purchase a life insurance policy you will name a beneficiary. This beneficiary has an insurable interest to the insured.

What is basic life salary?

UC provides basic life insurance coverage at no cost to all eligible employees. Basic Life provides life insurance equal to your annual base salary, up to $50,000. The coverage amount is based on your UC salary and appointment rate at the time of enrollment and as of January 1 of each subsequent year.

How is supplemental life insurance premium calculated?

The primary unit for figuring out a life insurance rate is the rate per thousand (cost per $1000 of insurance), which can vary depending on which factors influence it (age, gender, etc). For example, if the rate is $0.2 per $1,000 and an enrollee elects $15,000 in coverage, the monthly premium will be $3.

Is employer paid life insurance taxable to the employee?

The cost of employer-provided group-term life insurance on the life of an employee’s spouse or dependent, paid by the employer, is not taxable to the employee if the face amount of the coverage does not exceed $2,000. The entire amount is taxable, not just the amount that exceeds $2,000.

Can an employer be the beneficiary of a life insurance policy?

purpose, employees may want to name their employer as beneficiary of their group life insurance, especially when the employer is a charitable organization. Employers such as ERISA plan sponsors may want to discourage this practice since they are ERISA fiduciaries of the plan.

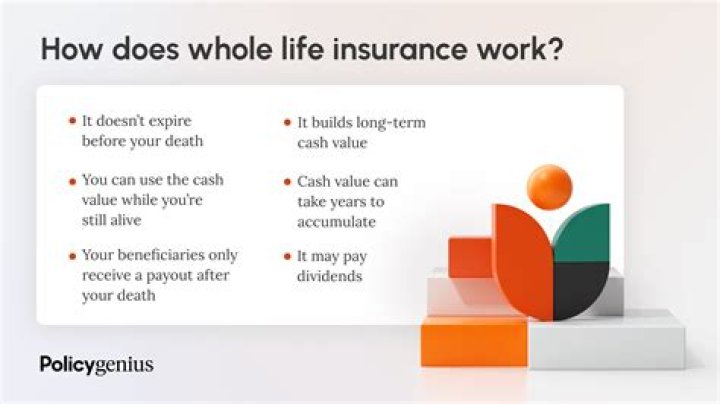

What happens when you buy whole life insurance?

When you buy a participating whole life insurance policy from a mutual insurance company you become a partial owner in the company. You now share in the profits and growth of the insurance company. You have voting rights. And you have the right to dividends paid out by the insurance company to your participating whole life policy.

Can a company offer life insurance to employees?

Group-term life insurance can be offered to employees only, not to their spouses and children. To take advantage of the tax deduction for group-term life insurance (i.e., the value of up to $50,000 in insurance is tax-exempt for the employee), you must have at least 10 full-time employees.

Who are the owners of Life Insurance Limited Liability Company?

The Life Insurance Limited Liability Company (LILLC) is a separate entity that operates independently from the underlying business and is specifically designed to own insurance contracts on the lives of the business owners. The owners who are the parties to the Buy Sell agreement are also the Members of the LILLC.

How are long term care benefits attached to whole life insurance?

Long-term care riders can be attached to permanent life insurance policies, such as IUL and Whole Life. The rider allows you to receive long-term care benefit payments to help you pay for long-term care services.