Can form 8804 be signed electronically?

No. The IRS supports electronic filing only for Form 1065 and related forms and schedules and the extension Form 7004. Any forms that are filed to the IRS separately from Form 1065, such as Form 8804, are not included in the electronic file and, therefore, must be filed on paper.

Can form 8804 be extended?

File Forms 8804 and 8805 separately from Form 1065. If you need more time, you can file Form 7004 to request an extension of time to file Form 8804.

What is effectively connected taxable income?

Generally, when a foreign person engages in a trade or business in the United States, all income from sources within the United States connected with the conduct of that trade or business is considered to be Effectively Connected Income (ECI).

Does IRS accept electronic signature?

State e-signatures Many states, including California, do not allow e-signatures for business tax returns. Other states, including New York, recently adopted laws allowing e-signatures for e-filed documents as a result of the pandemic and have their own requirements for identity verification (see N.Y.

Who must file a Form 1042?

Who Must File 1042-S? Any withholding agent (a person or institution, such as an employer, university, or business) that paid any amount subject to withholding to a foreign person must submit a 1042-S. The 1042-S is filed with the IRS and a completed copy is also sent to the employee or business.

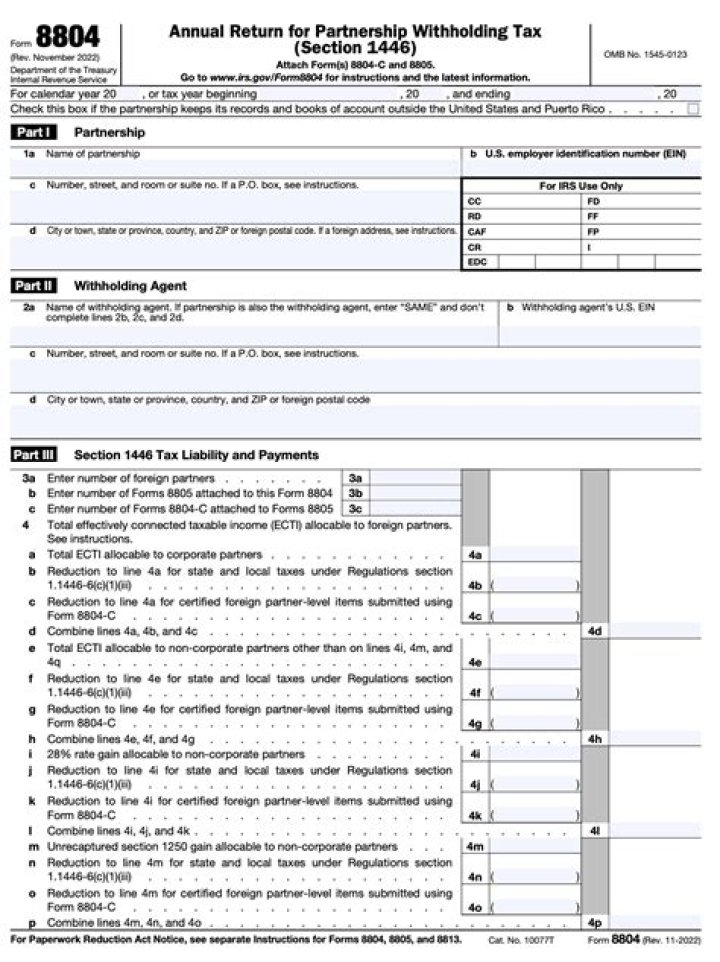

Which is the Transmittal Form for form 8804?

Use Form 8804 to report the total liability under section 1446 for the partnership’s tax year. Form 8804 is also a transmittal form for Form (s) 8805. Use Form 8805 to show the amount of ECTI and the total tax credit allocable to the foreign partner for the partnership’s tax year.

What do you need to know about ecti and applicable percentage?

ECTI and applicable percentage are defined later. For ease of reference, these instructions refer to various requirements applicable to withholding agents as requirements applicable to partnerships themselves. A partnership must determine if any partner is a foreign partner subject to section 1446.

Do you have to pay withholding tax on ecti?

A foreign or domestic partnership that has ECTI allocable to a foreign partner must pay a withholding tax equal to the applicable percentage of the ECTI that is allocable to its foreign partners. However, this requirement doesn’t apply to a partnership treated as a corporation under the general rule of section 7704 (a).

When to file Form 8804 for extension of time?

If you need more time, you can file Form 7004 to request an extension of time to file Form 8804. Note. Filing a Form 7004 doesn’t extend the time for payment of tax. File on or before the 15th day of the 4th, 6th, 9th, and 12th months of the partnership’s tax year for U.S. income tax purposes.