Can I still use 1099 Misc for non employee compensation?

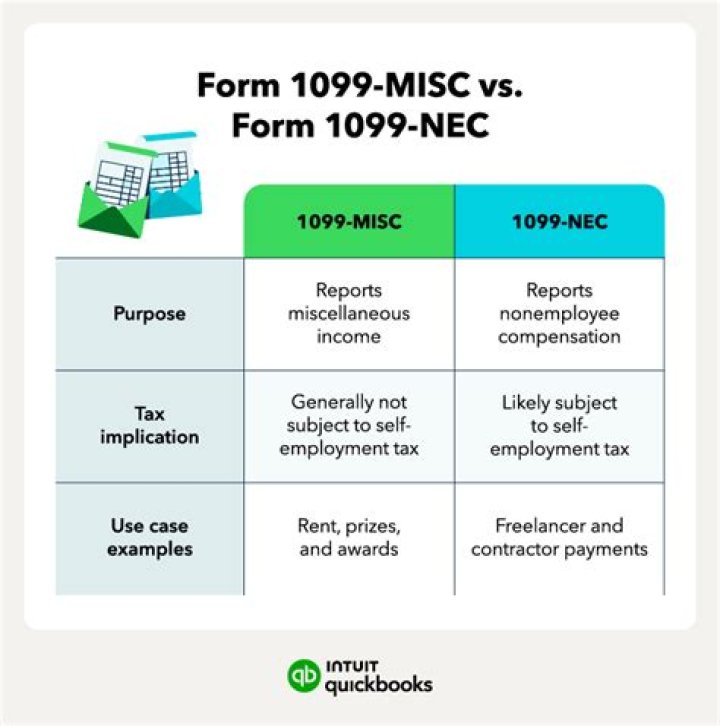

The Form 1099-NEC is used to report payments of compensation to non-employees for services rendered in the course of a trade or business, but where payments to non-employees are not for services they generally must be reported on Form 1099-MISC.

What qualifies as non employee compensation?

Nonemployee compensation (also known as self-employment income) is the income you receive from a payer who classifies you as an independent contractor rather than as an employee. This type of income is reported on Form 1099-MISC, and you’re required to pay self-employment taxes on it.

Which form should nonemployee compensation income be reported?

Form 1099-NEC

More In Forms and Instructions Use Form 1099-NEC to report nonemployee compensation.

When to report nonemployee compensation on Form 1099?

The PATH Act, P.L. 114-113, Div. Q, sec. 201, accelerated the due date for filing Form 1099 that includes nonemployee compensation (NEC) from February 28 to January 31 and eliminated the automatic 30-day extension for forms that include NEC. Beginning with tax year 2020, use Form 1099-NEC to report nonemployee compensation.

When to use form 1099-nec for non-employees?

Prior to 2020, if your small business hired independent contractors, you issued a 1099-MISC Form to report nonemployee compensation. For the tax year 2020, the IRS has reintroduced Form 1099-NEC (NEC stands for Non-Employee Compensation) to replace 1099-MISC.

Do you have to file Form 1099 Misc for nonqualified deferred compensation?

Nonqualified deferred compensation (box 14). You must also file Form 1099-MISC for each person from whom you have withheld any federal income tax (report in box 4) under the backup withholding rules regardless of the amount of the payment.

How to report payments to an attorney on form 1099-nec?

To report payments to an attorney on Form 1099-NEC, you must obtain the attorney’s TIN. You may use Form W-9, Request for Taxpayer Identification Number and Certification, to obtain the attorney’s TIN. An attorney is required to promptly supply its TIN whether it is a corporation or other entity, but the attorney is not required to certify its TIN.