Can partnerships deduct organizational costs?

In the taxable year in which a partnership begins business, an electing partnership may deduct an amount equal to the lesser of the amount of the organizational expenses of the partnership, or $5,000 (reduced (but not below zero) by the amount by which the organizational expenses exceed $50,000).

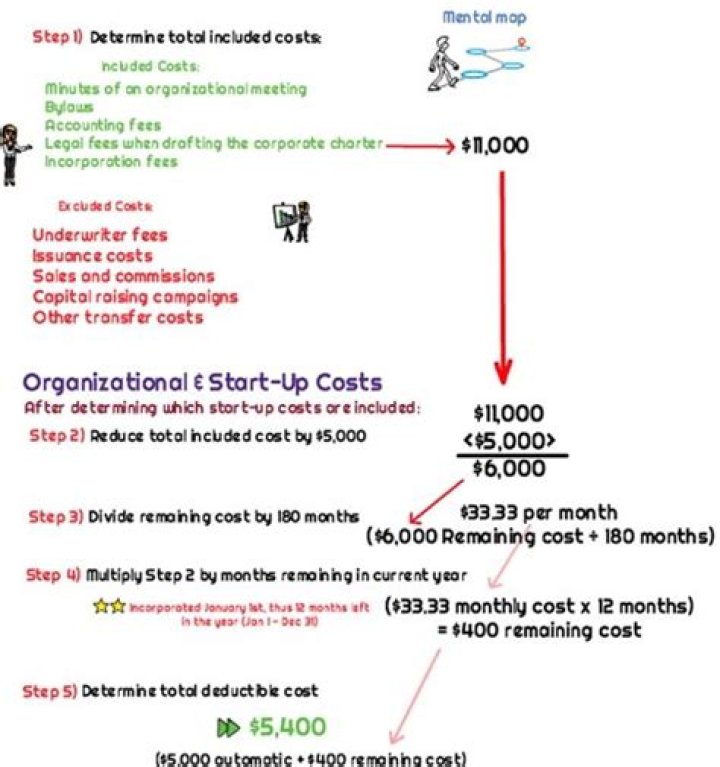

Do you amortize organizational costs?

If you decide to operate your business as a corporation, the corporation can elect to deduct up to $5,000 of its organizational expenditures and amortize the remainder over a period of 180 months. The $5,000 deducted for organizational expenses must be reduced by the amount by which the expenses exceed $50,000.

What are organizational expenses?

Definition: An organizational cost or expense is the initial cost incurred to create a company. Organizational costs usually include legal and promotional fees to establish the company with the state and federal government. In other words, organizational expenses are the costs of organizing or incorporating a company.

Under Sec. 709(b)(1)(A), a partnership can elect to deduct organizational expenses in the year in which the partnership begins business.

Organizational costs are expenses related to forming a corporation, partnership, or limited liability company (not a sole proprietorship). These may include legal, management, consulting, accounting and filing fees.

What are organizational expenses provide examples?

Examples of Organizational Costs Include:

- Legal services incident to the creation of the corporation, such as drafting of charters, bylaws, and minutes of meetings;

- Necessary accounting services;

- Fees paid for temporary directors and organizational meetings; and.

- Registration fees paid to the state of incorporation.

What do you need to know about IRS Form 1065?

Jean Murray, MBA, Ph.D., is an experienced business writer and teacher. She has written for The Balance on U.S. business law and taxes since 2008. IRS Form 1065 is the U.S. Return of Partnership Income used to report each partners’ share of income or loss of the business.

Can a limited liability company file a Form 1065?

Tax liability is passed through to the members who then pay taxes on the income on their personal returns. Limited Liability Companies (LLCs) can make an election with the IRS to be taxed as partnerships, and they would file Form 1065 in this case as well.

What is Form 1065 for Qualified Opportunity Fund?

To be certified as a qualified opportunity fund (QOF), the partnership must file Form 1065 and attach Form 8996, Qualified Opportunity Fund, even if the partnership had no income or expenses to report. See Schedule B question 26 and the Instructions for Form 8996.

Do you have to file Form 1065 for foreign partnership?

Foreign partnerships with income in the U.S. must also file Form 1065. As of 2018, foreign partnerships earning less than $20,000 in the country or partnerships that receive less than 1% of their income in the U.S. may not have to file. 5 Nonprofit religious organizations also file this form.