Can you be partially VAT registered?

Overview. Some goods and services are exempt from VAT. This means you cannot reclaim any VAT on your business purchases or expenses. If you are VAT-registered and incur VAT on any items that will be used to make exempt supplies, you are classed as partly exempt.

What is partial attribution?

A person who sells a mixture of taxable, exempt with credit and exempt without credit supplies must apply partial attribution. The rate of attribution is calculated annually and it is determined by value of supplies whose credits are allowed as a ratio of all supplies.

Do we charge VAT on fuel?

The supply of fuel, diesel and illuminating kerosene is specifically zero-rated in terms of sections 11(1)(h) and (l) of the VAT Act, read with Part 5A of Schedule 1 of the Customs and Excise Act. The zero-rating does not apply to liquid gas whether acquired for domestic or industrial use.

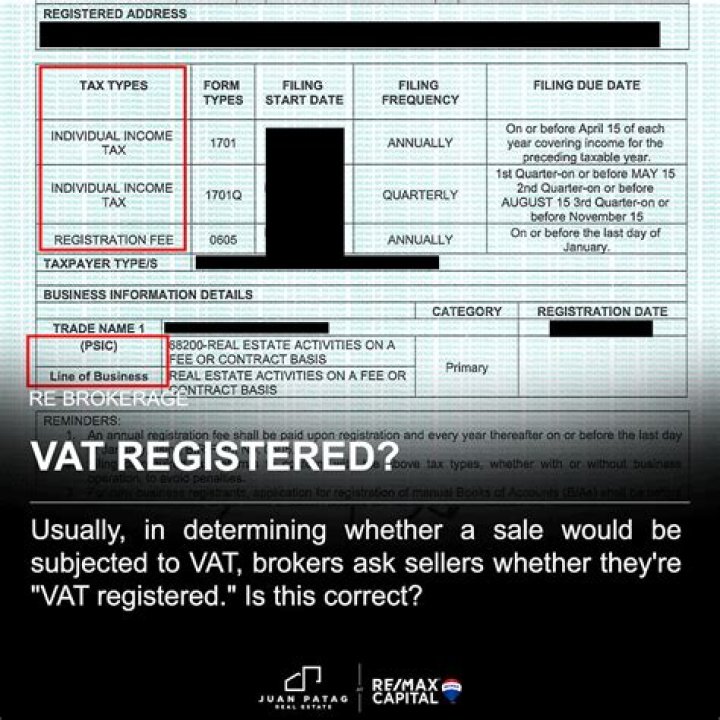

Who is VAT exempt in Malta?

Those businesses whose turnover is below the established entry threshold for their business activity may apply to register under Article 11 of the VAT Act in order to be exempted from charging VAT when supplying taxable goods or taxable services. As well as not being obligated to charge VAT, they may not recover VAT.

What is VAT exemption number?

VAT exemption can refer to either goods and services that are not subject to VAT or to organisations that cannot register for VAT. It’s important for companies to make sure that their invoices contain the correct information about taxes and VAT – even if they’re exempt.

Is arthritis VAT exempt?

You’ll not have to pay VAT when you buy medical or surgical appliances that are designed solely for the relief of a severe abnormality or severe injury such as amputation, rheumatoid arthritis, learning difficulties or blindness. Appliances that can be bought VAT-free include: invalid wheelchairs.

What is the difference between exempt supply and zero rated supply?

For a “zero-rated good,” the government doesn’t tax its sale but allows credits for the value-added tax paid on inputs. If a good or business is “exempt,” the government doesn’t tax the sale of the good, but producers cannot claim a credit for the VAT they pay on inputs to produce it.