Can you combine properties in a 1031 exchange?

IRC Section 1031 allows for the exchange of several properties into one or more replacement properties. Exchangers, however, need to be aware of the following rules that can make planning for such an exchange challenging: of the properties being sold. …

How often can you do 1031 exchange?

There’s no limit on how many times you can do a 1031. You can roll over the gain from one piece of investment real estate to another, then another and another. You may have a profit on each swap, but you avoid tax until you actually sell for cash. But be careful and do it right.

What do you need to know about Section 1031 exchanges?

To accomplish a Section 1031 exchange, there must be an exchange of properties. The simplest type of Section 1031 exchange is a simultaneous swap of one property for another. Deferred exchanges are more complex but allow flexibility. They allow you to dispose of property and subsequently acquire one or more other like-kind replacement properties.

How long does it take to replace a property in a 1031 exchange?

From the time of closing on the relinquished property, the investor has 45 days to nominate potential replacement properties and a total of 180 days from closing to acquire the replacement property. Identification requirements: The investor must identify the replacement property prior to midnight on the 45th day.

Is there an exception to IRC Section 1031?

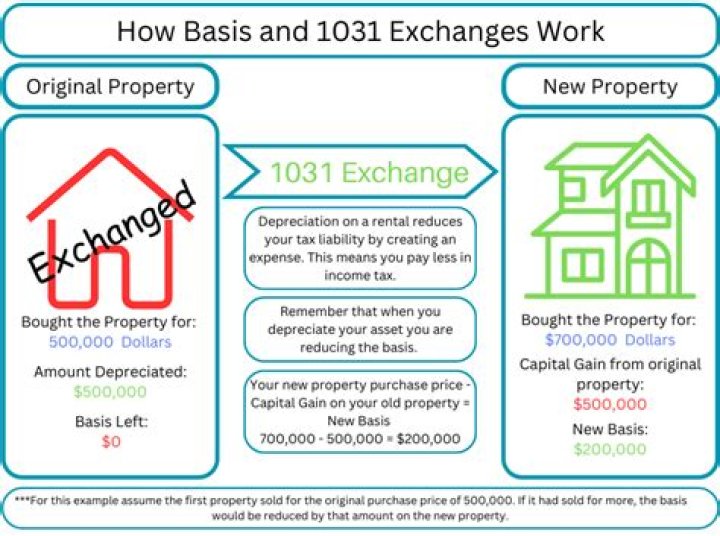

IRC Section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like-kind exchange.

Can a property be excluded from Section 1031?

No. The property of a taxpayer can be excluded from section 1031 even though used in a business or for investment purposes, under the following circumstances: Since property must be held for business or investment purposes in order to qualify, inventory is never deemed eligible property under section 1031.