Can you put term insurance in an Ilit?

An ILIT can own both individual and second to die life insurance policies. Second to die policies insure two lives and pay a death benefit only upon the second death.

What does Ilit mean?

irrevocable life insurance trust

An irrevocable life insurance trust (ILIT) is a trust that cannot be rescinded, amended, or modified, post creation. ILITs are constructed with a life insurance policy as the asset owned by the trust.

Is an Ilit a good investment?

Bottom Line. An ILIT is a good idea if you have a significant amount of wealth and assets you need to protect after you pass. To avoid hefty estate tax and creditors, as well as set up your family after you pass, an ILIT might work for you.

Why would you use an Ilit?

An ILIT provides a number of advantages beyond the ability to provide a tax-free death benefit. This includes protecting your insurance benefits from divorce, creditors and legal action against you and your beneficiaries. An ILIT also avoids probate and shields assets from expense and loss of privacy during probate.

Does life insurance go into a trust?

Trusts are not considered individuals; therefore, life insurance proceeds paid to trusts are generally subjected to estate tax. Also, the proceeds payable to a trust may not qualify for the inheritance tax exemption provided by some states for insurance payable to a named beneficiary.

Can a beneficiary be the trustee of an irrevocable trust?

Any individual may be a trustee and a beneficiary of a trust assuming that the trust agreement names other lifetime beneficiaries or successor beneficiaries after the death of the initial beneficiaries. For example, suppose a client wanted to serve as trustee of an irrevocable trust created for his benefit.

Can a beneficiary of an Ilit be the trustee?

Also, a beneficiary of an ILIT should generally not be a trustee. Therefore, you can choose a trusted professional advisor, friend or family member who is not a beneficiary or use a corporate fiduciary, such as a trust company or a bank’s trust department.

While you can use any term policy — either individual or group — to fund an ILIT, you may outlive it and render the ILIT useless. If you use a whole life policy and continue to pay the premiums, you are assured that the policy will be in place at your death.

Irrevocable Life Insurance Trust

What Is an Irrevocable Life Insurance Trust (ILIT)? An irrevocable life insurance trust (ILIT) is created to own and control a term or permanent life insurance policy or policies while the insured is alive, as well as to manage and distribute the proceeds that are paid out upon the insured’s death.

How much does an Ilit cost?

The set up fee for an ILIT is $200 and the annual base fee is $1,200 during lifetime of insured. There is no charge for the Annual Gift Letter (Crummey Notice). Additional fees include: $300 annual fee for each additional policy.

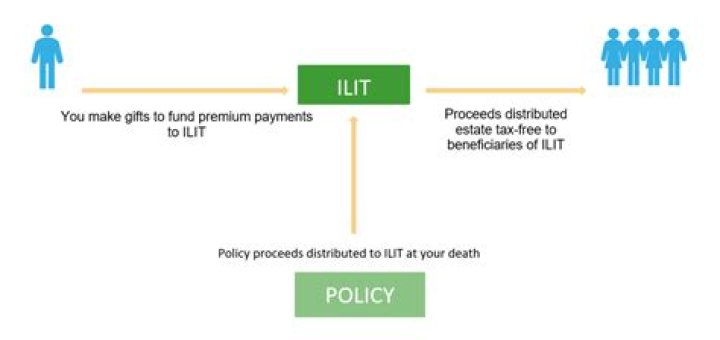

How does a life insurance trust ( Ilit ) work?

An ILIT is a type of living trust that’s specifically set up to own a life insurance policy. You can transfer ownership of an existing policy to the ILIT after it’s been formed, or the trust can purchase the policy directly.

Can a grantor change the terms of an Ilit?

ILITs are constructed with a life insurance policy as the asset owned by the trust. Once the grantor contributes property or life insurance death benefits to the trust, he or she cannot change the terms of the trust or reclaim any of the properties held within.

How are death benefits paid to an Ilit?

If properly structured, the death benefits paid to the ILIT will be free from inclusion in the gross estate of the insured. This differs from a scenario where life insurance death benefits are paid to an individual, because the proceeds are included in the taxable estate of the decedent.

How does an Ilit help you avoid estate taxes?

An ILIT can help you avoid estate taxes. Many people aren’t aware that for tax purposes, their estates might include the proceeds from their life insurance policies when they die. Depending on the value of the policy, this could invite an estate tax bill.