Can you take a loss on a variable annuity?

It is possible to deduct a variable annuity loss. There is some disagreement, however, over where on the tax return to deduct the loss. To deduct the loss, the annuity has to be sold (liquidated).

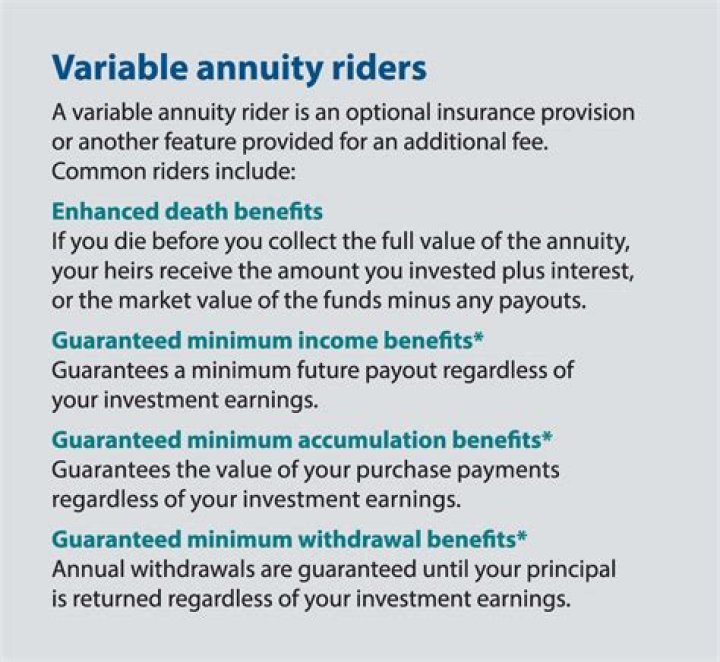

What is a rider on a variable annuity?

Riders are optional enhancements that are available on your annuity contract at an additional cost. They allow your financial professional to tailor your contract and help protect what’s most important to you. Please keep in mind that riders may not be available on all products.

What is a key advantage to living benefit variable annuities?

The Living-Benefit Feature The living benefit—as the name suggests—is intended to guarantee the benefit provided, and toward that end, it usually offers guaranteed protection of the principal investment and the annuity payments or guarantees a minimum income over a specified period to you and your beneficiary.

Do variable annuities have higher fees?

Variable annuities have investment and management fees. These fees can be referred to as expense ratios, 12b-1 fees or service fees. They can range from 0.6 percent to more than 3 percent each year.

What do variable annuities provide?

A typical variable annuity offers three basic features not commonly found in mutual funds: tax-deferred treatment of earnings; a death benefit; and. annuity payout options that can provide guaranteed income for life.

Can a loss be claimed on a variable annuity?

While non-qualified variable annuity account losses cannot be claimed within a year whereby the contract remains in force, it may be possible to claim a tax deduction for losses experienced when a lump-sum distribution is taken.

What do you need to know about variable annuities?

A variable annuity is a contract between you and an annuity provider — usually an insurance company — in which you purchase the ability to receive a stream of income for your life or a set period of time.

Is there a free look period for variable annuities?

Most variable annuity contracts have a “free look” period. It’s a test run on the annuity for you to determine if it’s right for your situation. This is a time of 10 or more days in which you can cancel your contract without paying surrender fees.

How does a tax deferred variable annuity work?

Variable annuities are tax-deferred vehicles which mean under current tax laws, any guaranteed interest rate or gain in an annuity is not taxable until you begin to actually receive this income. The power of tax-deferred variable annuities is the effect of “triple-compounding” on your retirement plan’s growth.