Do I have to take an RMD if I am still working?

Yes, even if you continue working past age 72,* you have to take an RMD from your IRA. However, you may qualify for an exception from taking RMDs from your current employer-sponsored retirement account, such as a 401(k), 403(b), or small-business account, if: You’re still working.

Are non-qualified plans subject to RMD?

The RMD rules cover all qualified retirement plans, including traditional IRAs and employer-sponsored plans such as 401(k)s. Original beneficiaries of Roth IRAs don’t have to take RMDs, but beneficiaries who inherit Roth IRAs must take RMDs. Traditional IRAs don’t qualify for an RMD exception.

What do you do with RMD money you don’t need?

If you don’t need the RMD, consider investing the money in a taxable account or, if eligible, a Roth IRA or traditional IRA. Of note, for those who have inherited IRAs and who are taking RMDs these tactics can go a long way toward increasing wealth.

What are the RMD rules for a non-qualified annuity?

RMD Rules on a Non-Qualified Annuity. These annuities may also allow pre-funding of your retirement savings. Such annuities are referred to as “deferred annuities.”. A deferred annuity that is non-qualified works very differently from an annuity designed to work inside of a qualified plan, such as an IRA.

When do you have to repay a qualified disaster distribution?

Participants may also repay qualified disaster distributions within three years of receiving a distribution by making one or more contributions to an eligible retirement plan. Any repayment is treated as a trustee-to-trustee transfer.

Is there a way to avoid the RMD?

Many retirees and others need the income anyway, so avoiding the RMD is not a big deal. Others, however, don’t need the money and would prefer not to pay the tax on these distributions. For those who are working, there can be a way to avoid some or all of their RMD obligations.

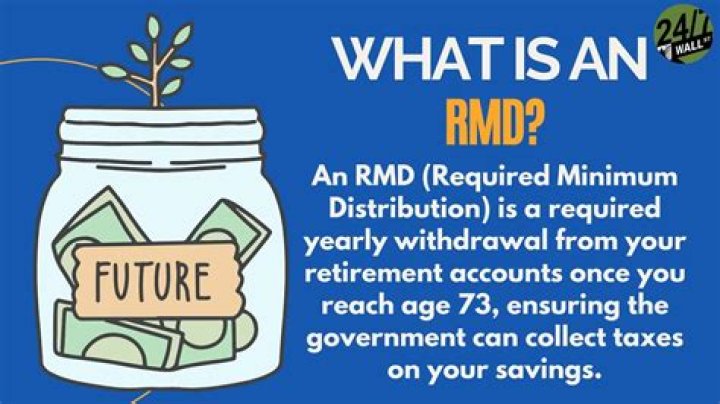

When do you have to take required minimum distributions?

Required Minimum Distributions (RMDs) generally are minimum amounts that a retirement plan account owner must withdraw annually starting with the year that he or she reaches 72 (70 ½ if you reach 70 ½ before January 1, 2020), if later, the year in which he or she retires.