Do you amortize original issue discount?

Tax Reporting The legal structure of the original issue discount is designed to prevent manipulation of taxes and interest income. Since the income is amortized through the life of the bond, as opposed to calculated on maturity, purchasers of the OID are unable to defer income recognition.

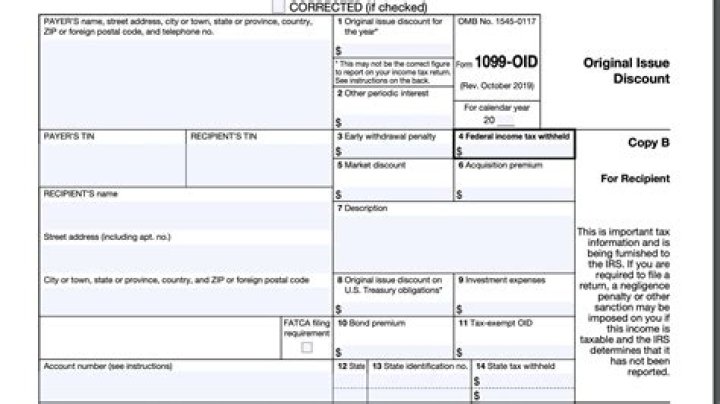

What is tax-exempt OID?

Box 8 shows the Original Issue Discount (OID) amount on a U.S. Treasury obligation for portion of the tax year that the taxpayer owned the Treasury obligation. This amount should be reported on the federal return as interest income but it is considered exempt from taxation for state and local income tax purposes.

How do I get a market discount on my tax return?

Rather, your form 1099-B for the disposition of the security will report the total accrued market discount in box 1f. You can then follow the instructions on Form 8949 with regard to presenting this amount on your personal income tax return as interest.

How is an original issue discount bond OID different from a zero-coupon bond?

That’s a bit like how an original issue discount (OID) works. When you buy an OID bond, you buy it for less than its face value. But then when the bond reaches maturity, the issuer pays you the full face value. So in the case of zero-coupon bonds, the bond doesn’t produce any income until it reaches maturity.

Where do I enter original issue discount on tax return?

Box 11 contains the Tax-exempt obligation or debt instrument Original Issue Discount amount. Generally this is reported as tax-exempt interest on the tax return on Form 1040, Line 8b.

What is original issue price?

An original issue discount (OID) is the discount in price from a bond’s face value at the time a bond or other debt instrument is first issued. The OID is the amount of discount or the difference between the original face value and the price paid for the bond.

When is the original issue discount ( OID ) taxable?

Get the latest info Original issue discount (OID) is a form of interest. It usually occurs when companies issue bonds at a price less than their redemption value at maturity. The difference between these two amounts is the OID. For bonds issued after 1984, the OID is treated as interest. It’s taxable as it accrues over the term of the bond.

How is acquisition premium related to OID income?

Acquisition premium is the excess of a debt instrument’s adjusted basis immediately after purchase, including purchase at original issue, over the debt instrument’s adjusted issue price at that time. A purchaser reduces any OID income by the acquisition premium, as discussed under Information for Owners of OID Debt Instruments, later.

Where do I find the Oid on my tax return?

This form shows the amount of OID (Box 1) to include in your income. Sometimes you might need to recalculate the OID. Ex: You bought the bond after the date it was originally issued, and you paid a premium for it. To learn more, see Publication 1212: Guide to Original Issue Discount (OID) Instruments at

Which is an example of an original issue discount?

What is an ‘Original Issue Discount – OID’. An original issue discount (OID) is the discount from par value at the time a bond or other debt instrument is issued; it is the difference between the stated redemption price at maturity and the actual issue price. The most extreme example of an OID is a zero-coupon bond.