Does depreciation change basis?

Your basis in an asset generally does not change over time. A different percentage is applied to the original basis calculation to determine each year’s depreciation deduction. this is the amount that will be recovered through depreciation over the life of the asset.

What happens when you make a change in estimate depreciation?

If there is a significant change in an asset’s estimated salvage value and/or the asset’s estimated useful life, the change in the estimate will result in a new amount of depreciation expense in the current accounting year and in the remaining years of the asset’s useful life.

Is it OK to change the depreciation charges on an asset?

A company may decide to change the depreciation method it applies to a fixed asset. The change of accounting estimate alters the pace at which depreciation accumulates and thus affects the carrying value of asset — purchase cost less accumulated depreciation — on the balance sheet over time.

How does depreciation affect cost basis?

Depreciation will play a role in the amount of taxes you’ll owe when you sell. Because depreciation expenses lower your cost basis in the property, they ultimately determine your gain or loss when you sell. If you hold the property for at least a year and sell it for a profit, you’ll pay long-term capital gains taxes.

Can I change depreciation policy?

As per the Accounting Standard 1- Disclosure of Accounting Policies, the change in the method of depreciation is a change in the accounting estimate. Thus, the method of depreciation can be changed without retrospective effect or with retrospective effect.

Is there a change in the method of depreciation?

Not Accounting-Method Changes. Further, a change in the convention of a depreciable or amortizable asset is not a change in the asset’s placed-in-service date and, thus, is not an accounting-method change. Additionally, the final regulations provide examples of a change in a placed-in-service date.

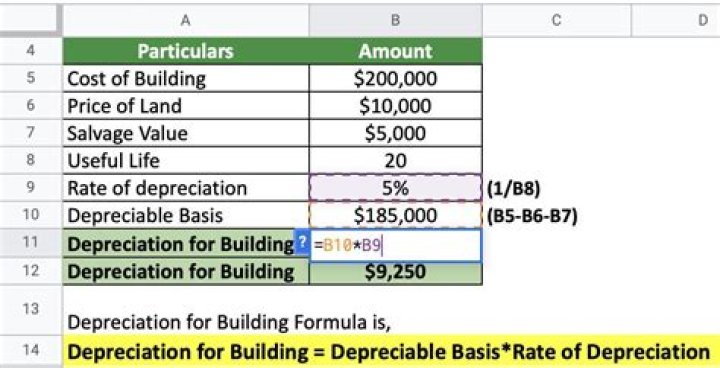

Which is the correct definition of depreciation basis?

What is Depreciation Basis? Depreciation basis is the amount of a fixed asset’s cost that can be depreciated over time. This amount is the acquisition cost of an asset, minus its estimated salvage value at the end of its useful life. Acquisition cost is the purchase price of an asset, plus the cost incurred to put the asset into service.

How do you correct a depreciation accounting error?

Depreciation errors are corrected by either filing an amended return or filing a change in accounting method form. Depreciation errors that are NOT subject to the accounting method change filing requirements require amended returns and include: You claimed the incorrect amount because of a mathematical error made in any year.

How does section 4.01 relate to depreciation?

Section 4.01 was added to clarify that a change from an impermissible method of determining depreciation for depreciable property in two or more consecutively filed Federal tax returns is an accounting-method change under Sec. 446 (e) and Regs. Sec. 1.446-1 (e).