Does my tax return say cash or accrual?

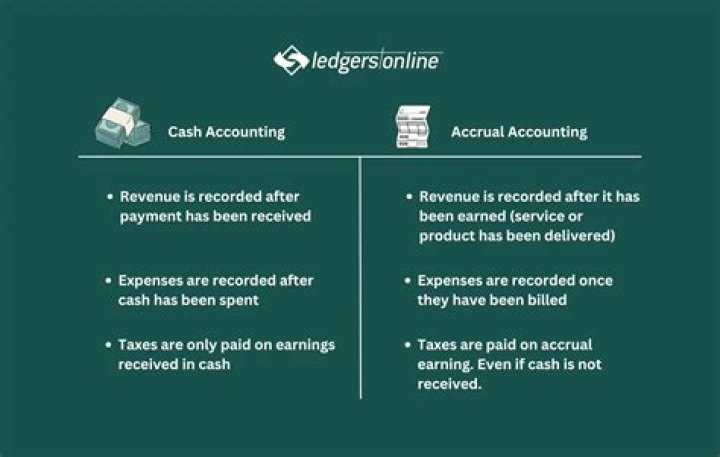

Under the cash method, you generally report income in the tax year you receive it, and deduct expenses in the tax year in which you pay the expenses. Under the accrual method, you generally report income in the tax year you earn it, regardless of when payment is received.

How do you report accrual income?

Accrued Income Reported on the Balance Sheet The amount of accrued income that a corporation has a right to receive as of the date of the balance sheet will be reported in the current asset section of the balance sheet. It could be described as accrued receivables or accrued income.

How do you choose between cash and accrual accounting?

The difference between cash and accrual accounting lies in the timing of when sales and purchases are recorded in your accounts. Cash accounting recognizes revenue and expenses only when money changes hands, but accrual accounting recognizes revenue when it’s earned, and expenses when they’re billed (but not paid).

Can a business switch from cash to accrual accounting?

If your business is eligible for both the cash and accrual methods, ask your tax advisor whether switching methods would lower your taxes. Depending on your circumstances, changing accounting methods may require IRS approval.

When to use cash or accrual for tax purposes?

Generally, a business is permitted to use the cash method of accounting for tax purposes unless it’s 1) expressly prohibited from using the cash method, or 2) expressly required to use the accrual method.

Can a C corporation use the cash method?

Businesses prohibited from using the cash method include C corporations and partnerships with a C corporation partner, unless one of the following exceptions applies: The business’s average annual gross receipts for the previous three tax years are $5 million or less.

What kind of Business is required to use accrual method?

The following types of businesses generally are required to use the accrual method: Businesses with income from long-term contracts (such as construction firms and manufacturers), which generally must use the percentage-of-completion method. Businesses with inventories, with certain exceptions. (See “A note on inventories.”)