Does NY allow NOL carryforward?

As a result of New York’s decoupling, for New York income tax and NYC Business Tax purposes, taxpayers will only be allowed to carryback NOLs for 2 years and the NOLs can only offset 80% of income.

Does the CARES Act carry over to 2021?

The CARES Act increases this ceiling to 100% for 2020. Barring further legislation, the ceiling will revert to 60% of AGI for 2021 through 2025. Then it’s scheduled to revert to 50% of AGI, starting in 2026. The CARES Act also authorized a deduction of up to $300 for cash donations by individuals who don’t itemize.

As a result of New York’s decoupling, for New York income tax and NYC Business Tax purposes, taxpayers will only be allowed to carryback NOLs for 2 years and the NOLs can only offset 80% of income. For tax years beginning in 2019 and 2020, the CARES Act raises the threshold to 50% of adjusted taxable income.

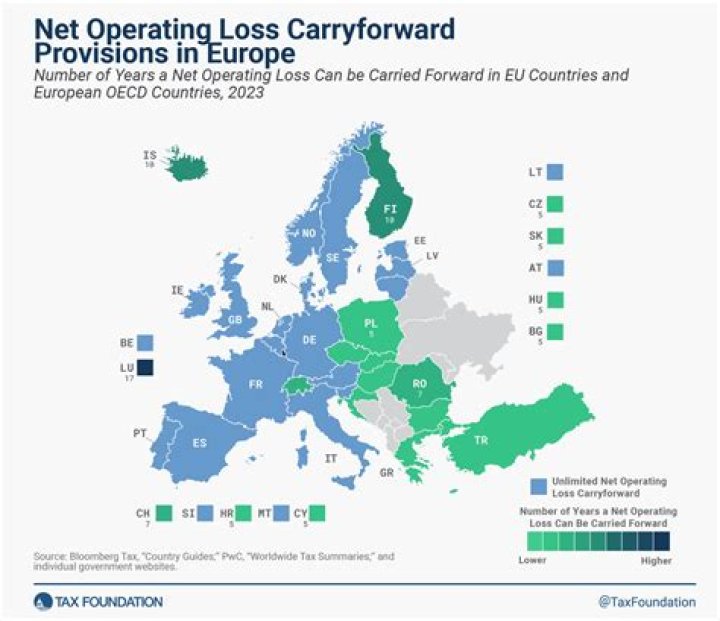

How long can corporate NOL be carried forward?

NOLs may now be carried forward indefinitely until the loss is fully recovered, but they are limited to 80% of the taxable income in any one tax period.

Where do I file CT 3 in NY?

NYS CORPORATION TAX.

How far can you carry back corporation tax losses?

three years

For trade losses of tax years 2020 to 2021 and 2021 to 2022 it is intended to provide additional relief by allowing unrelieved losses to be carried back and set against profits of the same trade for three years before the tax year of the loss.

How are NOL carryovers handled in New York?

For NOL carryovers incurred prior to 2015, New York has created a Prior Net Operating Loss Conversion (PNOLC) Subtraction to allow for utilization of these NOLs. The PNOLC is converts pre-2015 NOLS into post apportionment NOLs by applying taxpayer’s 2014 allocation percentage to them. The result is then divided by 6.5.

Where do I Find my Nol carryforwards for 2015?

Taxpayers must use their NOL carryforwards from tax years prior to 2015 to compute a PNOLC subtraction on the 2015 Form CT-3.3, Prior Net Operating Loss Conversion (PNOLC) Subtraction, and report the appropriate deduction on their Form CT-3 or CT-3-A, Part 3, line 16 for tax years 2015 and later.

Is the 20 year NOL carry forward affected by tax reform?

The 20-year NOL carry forward period was not impacted by the tax reform. W&G Observation: This modification is a welcome one for taxpayers as New York is now conforming with the Federal tax treatment of NOLs.

How long is the New York State Nol carryback period?

As set forth in New York Publication 145 (on page five), the New York State NOL carryback period mirrors the Federal, i.e. two years. In addition, the publication sets forth additional New York State NOL limitations that may be further exacerbated by The Act’s extended five year NOL carryback period per the below excerpt: