Does section 965 apply in 2018?

Taxpayers should be aware of their income tax obligations under section 965. The new tax applies to the last taxable year of specified foreign corporations beginning before January 1, 2018, and the tax is includible in the U.S. shareholder’s tax year in which or with which the specified foreign corporation’s year ends.

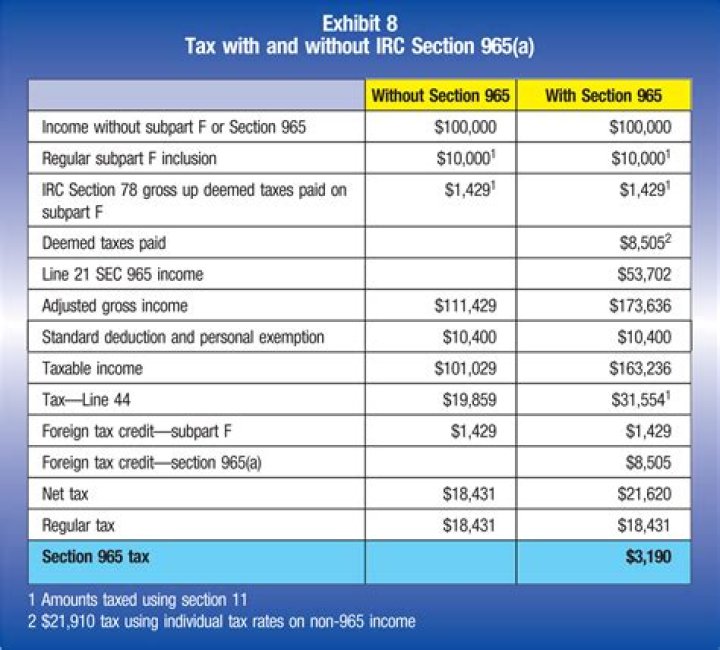

What is IRS Form 965 A?

This form is used to report a taxpayer’s net 965 tax liability for each tax year in which a taxpayer must report or pay section 965 amounts.

What is the 965 tax rate?

15.5 percent

Under section 965, corporations are expected to pay 15.5 percent transition tax on accumulated earnings and profits (E&P) related to cash assets. Other assets are subject to an 8 percent transition tax.

How do I make a 965 installment payment?

You may submit your section 965(h) net tax liability installment payment using any of the following payment options: EFTPS.gov (Web, IVR and Agent), credit cards, Direct Pay, bulk providers and batch providers.

Do I need to file Form 965 2019?

Form 965 as well as either Form 965-A (for individual taxpayers and entities taxed like individual taxpayers—for example, certain trusts and estates) or Form 965-B (for corporate taxpayers and REITS) must be attached to the 2019 income tax return.

When do you have to pay section 965 tax?

Taxpayers may have to pay tax resulting from section 965 of the Code when filing their 2017 tax returns. For example, section 965 of the Code may give rise to a 2017 tax liability for a calendar year United States shareholder holding an interest in a calendar year specified foreign corporation.

What do I need to file for IRC 965?

A person that has income under section 965 of the Code for its 2017 taxable year is required to include with its return an IRC 965 Transition Tax Statement, signed under penalties of perjury and, in the case of an electronically filed return, in Portable Document Format (.pdf) with a filename of “965 Tax”.

Where to find model statement for section 965?

A model statement is included in Appendix: Q&A3. Adequate records must be kept supporting the section 965 (a) inclusion amount, deduction under section 965 (c) of the Code, and net tax liability under section 965, as well as the underlying calculations of these amounts.

What was section 965 of the tax cuts and Jobs Act?

This action is prescribed by Internal Revenue Code (IRC) Section 965, which was enacted by Section 14103 of the Tax Cuts and Jobs Act (P.L. 115-97) (TCJA).