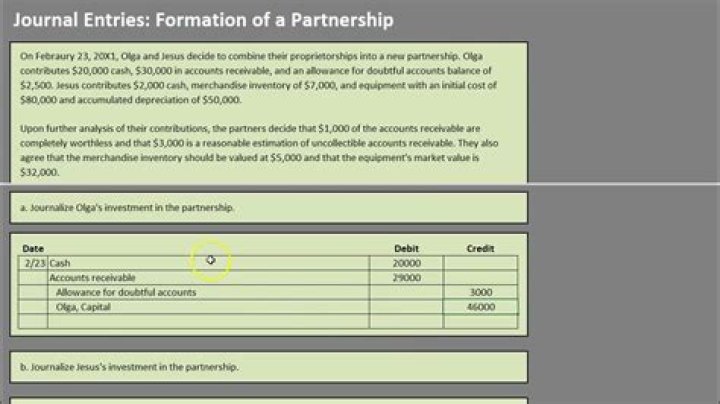

How are asset contributions of partners be recorded in the partnership books?

Assets contributed to the business are recorded at the fair market value. Anytime a partner invests in the business the partner receives capital or ownership in the partnership. You will have one capital account and one withdrawal (or drawing) account for each partner.

Who can deduct unreimbursed partnership expenses?

You can deduct unreimbursed partnership expenses (UPE) if you were required to pay partnership expenses personally under the partnership agreement. Don’t include any expenses you can deduct as an itemized deduction. Don’t combine these expenses with — or net them against — any other amounts from the partnership.

How would you record in the books of accounts assets taken over by a partner on dissolution?

Any asset of the firm taken over by the partner is recorded on the debit side and liability taken over is recorded on the credit side. Undistributed profits and reserves are recorded on the credit side and undistributed losses or fictitious assets are recorded on the debit side.

How is the basis of a partnership determined?

The partnership’s basis in its assets is determined based on the manner in which the partnership acquired the relevant asset. ●Assets contributed are contributed at the contributor’s basis. ●Assets sold are held based on the cost to the partnership. ●Rev.

When does a partner contribute property to a partnership?

When a partner contributes property to the partnership, the partnership’s basis in the contributed property = its fair market value ( FMV ). However, the outside basis of the partner increases only by the amount of the basis the partner had in the property.

What are the tax consequences of a partnership distribution?

Generally, there are no tax consequences of a current property distribution — there is never a taxable gain or loss, either to the partnership or to the partner. The partnership’s inside basis of the property carries over to become the partner’s basis, thereby reducing the partner’s outside basis by the carryover basis .

What happens when there is excess basis in a partnership?

If there is any excess basis over the partnership’s interest, then the assigned bases must be reduced by the excess. Any remaining allocable basis is then assigned to the remaining properties, reduced by any excess basis over the partner’s remaining interest.