How do I track a non deductible IRA?

If you are not able to deduct some or all of your contribution, you will need to file Form 8606 when you file your taxes. This form is important because it tracks all of your non-deductible contributions and establishes the cost basis in the IRA.

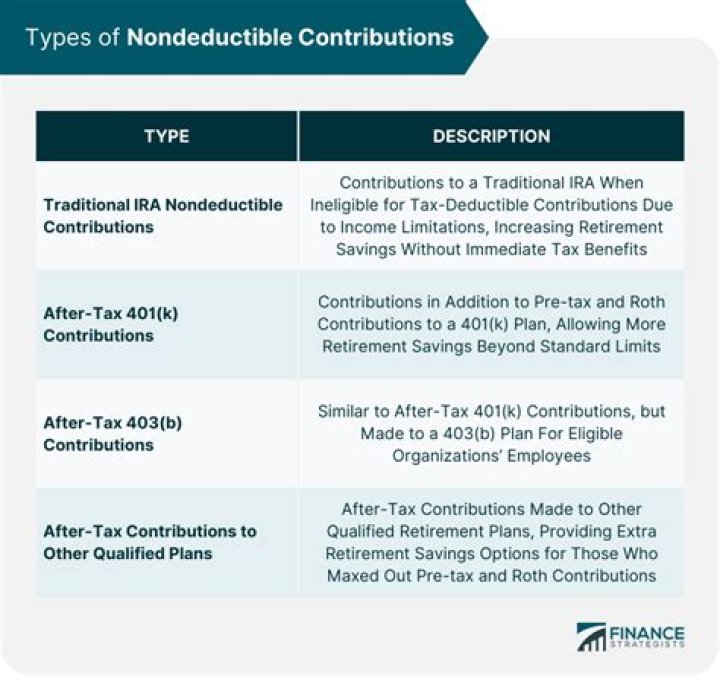

Do I need to track non deductible IRA contributions?

Any money you contribute to a traditional IRA that you do not deduct on your tax return is a “nondeductible contribution.” You still must report these contributions on your return, and you use Form 8606 to do so. Reporting them saves you money down the road.

What is basis for traditional IRA?

Basis. Your basis in traditional, SEP, and SIMPLE IRAs is the total of all your nondeductible contributions and nontaxable amounts included in rollovers made to these IRAs minus the total of all your nontaxable distributions, adjusted if necessary (see the instructions for line 2, later).

The easiest way to track and report your deductible and nondeductible IRA contributions is to complete and file Form 8606, “Nondeductible IRAs,” with your federal income tax return each year. Contact us with any questions you may have regarding your IRAs.

Are RMDs required on traditional IRAs?

If you have a Traditional, Rollover, Inherited, SEP, or SIMPLE IRA, you’ll need to take an RMD. RMDs are not required with Roth IRAs, unless you inherit a Roth IRA from a non-spouse. If you don’t take your RMD by the IRS deadline, you may be liable for a 50% penalty on insufficient or late RMD withdrawals.

Do I need to track cost basis for IRA?

Why cost basis usually isn’t important for an IRA In a taxable account, you only get taxed on the profit, and so measuring cost basis in order to calculate the appropriate tax is crucial. For a traditional IRA, though, most accountholders don’t have any cost basis as such.

What do you need to know about RMDs for IRA?

The IRS provides important taxpayer information about RMDs, including FAQs, a chart that highlights some of the basic RMD rules as applied to IRAs and defined contribution plans, and resources to help you accurately compute your annual RMDs.

When do you no longer include premium in RMD calculations?

When an IRA or 401k is annuitized you no longer include the premium or “value” of that annuity in future RMD calculations. The IRS considers such an IRA immediate annuity to have satisfied future RMDs (that is, only with respect to the amount of premium which was used to buy that IRA Annuity). I’ll have more to say about this later.

When to withdraw RMD from deferred fixed annuity?

If you purchase a deferred fixed annuity using Traditional IRA monies, then those monies will be subject to RMDs once you reach 70 ½. You can either withdraw the RMDs from the annuity, or withdraw the RMDs from some other Traditional IRA source.

What are the RMD rules for a non spouse inheriting an IRA?

RMD Rules When a Non-Spouse Inherits a Traditional IRA The SECURE Act , which passed at the end of 2019, raised the RMD age from 70.5 to 72. But it also essentially eliminated the “stretch IRA” option for non-spouse inheritors of IRAs.