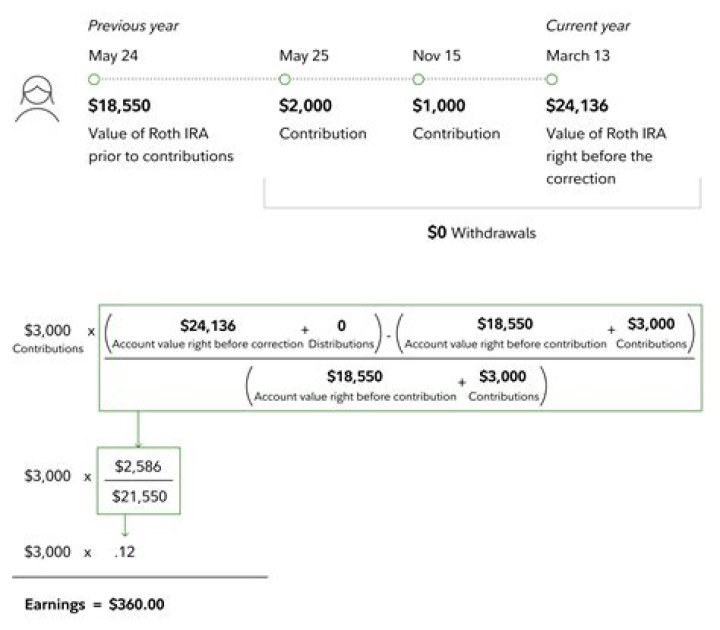

How do I track my Roth IRA contributions?

You’ll have to track your contributions or have your account manager send you a statement. If you convert another account to a Roth, you will get a Form 5498 from the account manager showing how much money you moved to the Roth. You report conversions to the IRS on Form 8606.

What should my Roth contribution be?

The total annual contribution limit for the Roth IRA is currently $6,000, with an additional catch-up contribution of up to $1,000 allowed for people 50 or older. That limit applies to both Roth and traditional IRA accounts; if you have both, you can contribute a total of up to $6,000 ($7,000 if 50 or older).

How much should I contribute to my Roth IRA each month?

The IRS, as of 2021, caps the maximum amount you can contribute to a traditional IRA or Roth IRA (or combination of both) at $6,000. Viewed another way, that’s $500 a month you can contribute throughout the year. If you’re age 50 or over, the IRS allows you to contribute up to $7,000 annually (about $584 a month).

When do you have to make contributions to a Roth IRA?

A Roth IRA can be established at any time. However, contributions for a tax year must be made by the IRA owner’s tax-filing deadline, which is generally April 15 of the following year. Tax-filing extensions do not apply. There are two basic documents that must be provided to the IRA owner when an IRA is established:

Can a qualified retirement plan contribute to a Roth IRA?

Also, the fact that you participate in a qualified retirement plan has no bearing on your eligibility to make Roth IRA contributions. So if you have the money and meet the income limitations, you can contribute to a 401 (k) plan at work and then contribute to your own Roth IRA. Roth IRA Income Limits

Can a person with no income contribute to a Roth IRA?

Only earned income can be contributed to a Roth IRA. You can contribute to a Roth IRA only if your income is less than a certain amount.

What are the sources of funding for a Roth IRA?

A Roth IRA can be funded from a number of sources: 1 Regular contributions 2 Spousal IRA contributions 3 Transfers 4 Rollover contributions 5 Conversions