How do you account for stolen inventory?

How to Account for Lost Inventory on an Income Statement

- Count the total units of lost inventory.

- Decide whether the loss was small or large relative to your total sales.

- Decide whether the loss was normal or unusual.

- Add small and normal inventory losses to the cost of your goods sold.

How do you calculate the cost of stolen inventory?

Subtract the cost of goods sold from the cost of goods available for sale to estimate the ending inventory. This is the lost inventory if the catastrophe has caused extensive damage to your warehouse and you have to replace the entire inventory.

What is stolen inventory?

Stolen inventory is the big loss of any organisation who does the business of physical products. Products can be stolen at any time from production to sale process.

How do you record inventory purchase in accounting?

Under the periodic system, the company can make the journal entry of inventory purchase by debiting the purchase account and crediting accounts payable or cash account. The purchase account is a temporary account, in which its normal balance is on the debit side.

How do you record a inventory write off?

Using the direct write-off method, a business will record a credit to the inventory asset account and a debit to the expense account. For example, say a company with $100,000 worth of inventory decides to write off $10,000 in inventory at the end of the year.

Can you write up inventory IFRS?

IFRS requires that inventory is carried at the lower of cost or net realizable value; U.S. GAAP requires that inventory is carried at the lower of cost or market value. IFRS allows for some inventory reversal write-downs; GAAP does not.

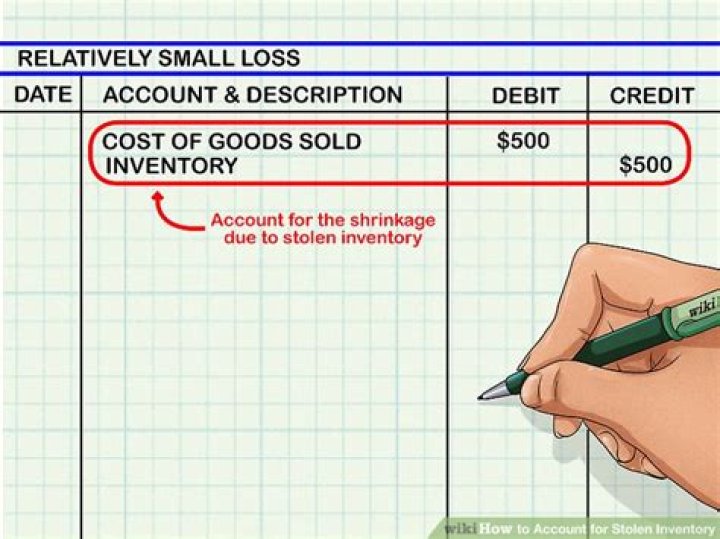

Account for the stolen inventory by debiting cost of goods sold for the value of inventory, $500, and crediting inventory for the same amount.

Is inventory an expense when purchased?

When you purchase inventory, it is not an expense. Instead you are purchasing an asset. When you sell that inventory THEN it becomes an expense through the Cost of Goods Sold account. You will understate your assets because your inventory won’t actually show up as inventory on the balance sheet.

Can you write off inventory purchases?

Inventory isn’t a tax deduction. Most people mistakenly believe that inventory is a line-item that they can deduct on their taxes. Inventory is a reduction of your gross receipts. This means that inventory will decrease your “income before calculating income taxes” or “taxable income.”

What’s the best way to account for stolen inventory?

Account for the stolen inventory by debiting cost of goods sold for the value of inventory, $500, and crediting inventory for the same amount. Include a note along with the adjusting entry. After making the entry, make sure to enter a note that indicates the entry was made to adjust for inventory shrinkage.

When do you exclude the cost of stolen goods?

If the computation of the closing balance of inventory under such system excludes the amount of inventory lost or stolen, no separate accounting entry would be necessary as the cost of goods sold would increase as a result of the reduction in closing stock thereby reflecting the impact of lost or stolen goods.

How is book value of inventory affected by stolen inventory?

Take the inventory report of book value of inventory with its book quantity of stock. Now, special staff will compare book value and quantity of stock with actual value and quantity of stock. If book value and quantity of stock is more than actual quantity and value stock, difference will be the loss due to stolen inventory.

What’s the difference between inventory and cost of goods sold?

Merchandise inventory is the cost of goods on hand and available for sale at any given time. Merchandise inventory (also called Inventory) is a current asset with a normal debit balance meaning a debit will increase and a credit will decrease. To determine the cost of goods sold in any accounting period, management needs inventory information.