How do you calculate cost of goods sold for inventory?

The cost of goods sold formula is calculated by adding purchases for the period to the beginning inventory and subtracting the ending inventory for the period. The beginning inventory for the current period is calculated as per the leftover inventory from the previous year.

Which inventory valuation method would you choose to calculate the cost of goods sold and closing inventory?

First-In, First-Out (FIFO) It is one of the most common methods of inventory valuation used by businesses as it is simple and easy to understand. During inflation, the FIFO method yields a higher value of the ending inventory, lower cost of goods sold, and a higher gross profit.

How does cost of goods sold affect inventory?

Inventory that is sold appears in the income statement under the COGS account. COGS only applies to those costs directly related to producing goods intended for sale. The balance sheet has an account called the current assets account. Under this account is an item called inventory.

Which one out of the following is not an inventory valuation method?

EOQ is not an inventory valuation method. Economic order quantity (EOQ) is the ideal order quantity a company should purchase for its inventory given a set cost of production, a certain demand rate, and other variables.

How do you find the cost of goods sold?

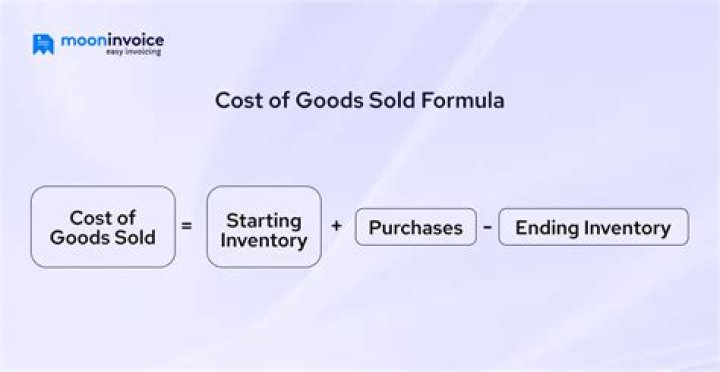

The basic formula for cost of goods sold is:

- Beginning Inventory (at the beginning of the year)

- Plus Purchases and Other Costs.

- Minus Ending Inventory (at the end of the year)

- Equals Cost of Goods Sold. 4

Is inventory valuation cost of goods sold?

Inventory valuation is the cost associated with an entity’s inventory at the end of a reporting period. It forms a key part of the cost of goods sold calculation, and can also be used as collateral for loans. This valuation appears as a current asset on the entity’s balance sheet.

How are cost of goods sold and inventory valuation calculated?

With the Weighted Average Cost inventory valuation method, inventory, and Cost of Goods Sold (COGS) are calculated based on the average cost of all items purchased during a period. This method is mainly used by businesses that don’t have variation in their inventory. Weighted Avg Cost Valuation: Example 1 Average Cost Inventory Method

Which is the best method for valuing inventory?

Method Description LIFO Last-in, first-out method of valuing inventory, which assumes that the most recently purchased units are sold first LIFO assumes that the cost of the last items purchased is assigned to the first items sold, and that the cost of ending inventory is the cost of the merchandise purchased earlier.

How is weighted average cost used in inventory valuation?

The weighted average cost (WAC) method of inventory valuation uses a weighted average to determine the amount that goes into COGS and inventory. The weighted average cost method divides the cost of goods available for sale by the number of units available for sale. The WAC method is permitted under both GAAP and IFRS.

How is the cost of ending inventory calculated?

Inventory: Special Topics – Inventory Valuation Methods 5 FIFO assumes that the cost of the first items acquired is assigned to the first items sold. The cost of ending inventory is the cost of the merchandise purchased most recently.