How do you calculate FIFO average cost?

It is calculated by dividing the total number of units you have on hand by the total cost of goods. You will arrive at an average unit cost for each unit of your inventory.

Is LIFO the same as average cost?

Producing goods generally becomes more expensive as time passes, so LIFO generally leads to a lower inventory value and higher cost of goods sold compared with the weighted-average method. The U.S. requires businesses to use the same inventory methods for reporting and tax purposes.

How do you calculate the average cost method?

Also referred to as the weighted average cost method, the average-cost method is an accounting formula used when calculating inventory value. This figure is reached by dividing the total cost of goods by the total number of goods over a specific accounting cycle.

Average Cost Method of accounting for inventory takes an average, as the name implies, of all of the costs of all of your inventory. It is calculated by dividing the total number of units you have on hand by the total cost of goods. You will arrive at an average unit cost for each unit of your inventory.

The average cost is computed by dividing the total cost of goods available for sale by the total units available for sale. This gives a weighted-average unit cost that is applied to the units in the ending inventory.

How do you calculate LIFO?

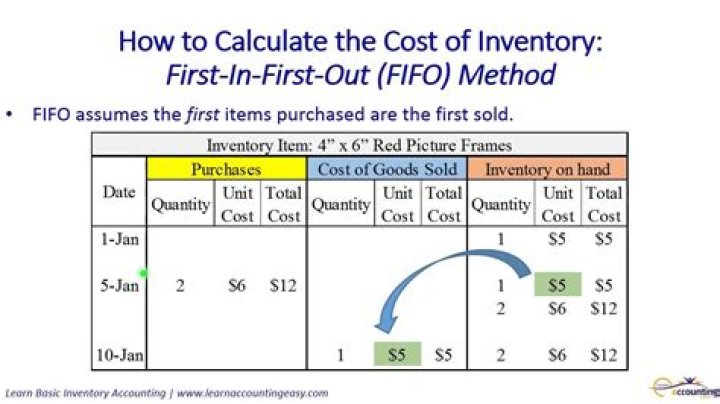

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Why LIFO method is used?

The LIFO method is used in the COGS (Cost of Goods Sold) calculation when the costs of producing a product or acquiring inventory has been increasing. Although the LIFO accounting method may mean a decrease in profits for a business, it can also mean less corporate tax a company has to pay.

How to calculate FIFO and LIFO accounting methods?

How to Calculate FIFO and LIFO. To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

Where can I find a FIFO calculator app?

Download FIFO & LIFO Calculator App for Your Mobile, So you can calculate your values in your hand. An online lifo fifo calculator allows you to calculate the remaining value of inventory and cost of goods sold by using the fifo and lifo method.

How to calculate cost of goods sold using FIFO?

To calculate COGS (Cost of Goods Sold) using the FIFO method, determine the cost of your oldest inventory. Multiply that cost by the amount of inventory sold. Please note: If the price paid for the inventory fluctuates during the specific time period you are calculating COGS for, that must be taken into account too. Let’s use an example.

Which is the opposite of FIFO and LIFO?

LIFO is the opposite of the FIFO method and it assumes that the most recent items added to a company’s inventory are sold first. The company will go by those inventory costs in the COGS (Cost of Goods Sold) calculation.