How do you calculate the beta of a stock using the covariance?

Covariance is used to measure the correlation in price moves of two different stocks. The formula for calculating beta is the covariance of the return of an asset with the return of the benchmark, divided by the variance of the return of the benchmark over a certain period.

How is the beta of a stock calculated?

A security’s beta is calculated by dividing the product of the covariance of the security’s returns and the market’s returns by the variance of the market’s returns over a specified period. The beta calculation is used to help investors understand whether a stock moves in the same direction as the rest of the market.

How do you calculate the covariance of a stock?

In other words, you can calculate the covariance between two stocks by taking the sum product of the difference between the daily returns of the stock and its average return across both the stocks.

What is good beta for stock?

A stock that swings more than the market over time has a beta above 1.0. If a stock moves less than the market, the stock’s beta is less than 1.0. High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

Does covariance have to be positive?

Covariance indicates the relationship of two variables whenever one variable changes. If an increase in one variable results in an increase in the other variable, both variables are said to have a positive covariance.

What is the maximum covariance?

With covariance, there is no minimum or maximum value, so the values are more difficult to interpret. For example, a covariance of 50 may show a strong or weak relationship; this depends on the units in which covariance is measured.

What is the covariance of returns between stock A and B?

Question: The covariance of the returns between Stock A and Stock B is 0.0087. The standard deviation of Stock A is 0.26, and the standard deviation of Stock B is 0.37.

What is difference between covariance and correlation?

Correlation is a measure used to represent how strongly two random variables are related to each other. Covariance is nothing but a measure of correlation. Correlation refers to the scaled form of covariance. Covariance indicates the direction of the linear relationship between variables.

What is the difference between covariance and correlation?

Covariance is nothing but a measure of correlation. Correlation refers to the scaled form of covariance. Covariance indicates the direction of the linear relationship between variables. Correlation on the other hand measures both the strength and direction of the linear relationship between two variables.

How to calculate the beta of a stock?

The way to calculate beta with covariance and variance, is that you get the covariance of the selected stock’s return to the market’s return, and divide this by the variance of the selected market’s return. Beta = COVARIANCE (Stock Returns, Market Returns) / VARIANCE (Market Returns) Using regression analysis to calculate beta

How is beta related to covariance and correlation?

Beta = Covariance stock versus market returns / Variance of the Stock Market See above for calculation of covariance. ρ is the correlation coefficient between the security / portfolio and the market. The correlation coefficient between FGH and the market is 0.8 Covariance of stock versus market returns is 0.8 x 6 x 4 = 19.2

How is the beta coefficient used in investing?

The Beta coefficient is a measure of sensitivity or correlation of a security or investment portfolio to movements in the overall market. We can derive a statistical measure of risk by comparing the returns of an individual security/portfolio to the returns of the overall market and identify the proportion…

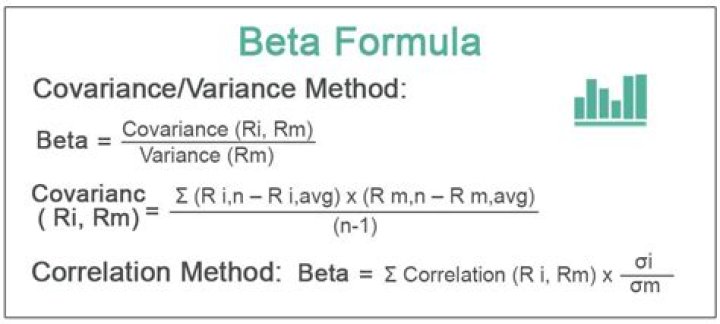

Which is the correct formula for the beta formula?

Beta Formula = Covariance (Ri, Rm) / Variance (Rm) Covariance( Ri, Rm) = Σ ( R i,n – R i,avg ) * ( R m,n – R m,avg ) / (n-1) Variance (Rm) = Σ (R m,n – R m,avg ) ^2 / n. To calculate the covariance, we must know the return of the stock and also the return of the market which is taken as a benchmark value.