How do you depreciate a new roof on a residential property?

Improvements are depreciated using the straight-line method, which means that you must deduct the same amount every year over the useful life of the roof. The IRS designates a useful life of 27.5 years, so, divide the total cost of the roof by 27.5 to reach the amount you are able to deduct each year.

Is a new roof tax deductible on rental property?

The cost of a new roof is an expense investment that most property owners hope they can get some relief from at tax time. However, the IRS does not allow full deductions for this type of expense when it is incurred.

How long do you depreciate a roof?

The IRS states that a new roof will depreciate over the course of 27.5 years for residential buildings and over the course of 39 years for commercial buildings.

Can you take bonus depreciation on a new roof?

Roofs do not qualify for “bonus” depreciation. That’s an additional depreciation deduction you can take for capital expenditures that exceed the $3,630,000 limit mentioned above. You can’t do it every year, but the 2020 tax year does qualify. Unfortunately roofing expenses do not qualify for this “bonus” depreciation.

Can I write off roof replacement?

Unfortunately you cannot deduct the cost of a new roof. Installing a new roof is considered a home improve and home improvement costs are not deductible. You will need to keep records of all home improvements made to increase the basis or determine the adjusted basis of your property.

When do you depreciate a new roof on a rental property?

Depreciation starts when you bring the new roof into service. If the property is tenanted, you bring the roof into service on the day you install it. If the property is unoccupied, you bring the roof into service when you next lease the rental property. Depreciation ends after 27.5 years, when you have fully recovered the cost of the new roof.

Can a landlord depreciate the cost of a home improvement?

They can also deduct the cost of improvements that have a useful life beyond one year on their tax return. The Internal Revenue Service lets landlords depreciate residential property improvements over a recovery period of 27.5 years.

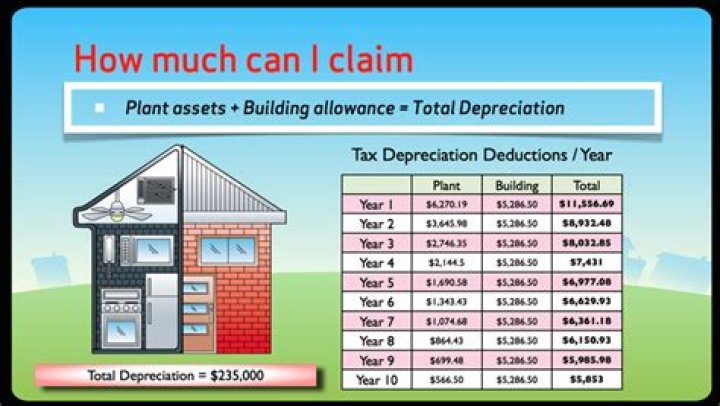

What is the general depreciation determination for residential rental property?

Following the issue of Interpretation Statement 10/01: Residential Rental Properties – depreciation of items of depreciable property (“IS 10/01”) in Tax Information Bulletin Vol 22 No 4 (May 2010) the Commissioner has issued a general depreciation determination to provide a new list for the “Residential Rental Property Chattels” industry category.

Can a landlord deduct the cost of a new roof?

Landlords can deduct one-year expenses, such as leasing agent’s fees, from the rent they receive thus reducing taxable income. They can also deduct the cost of improvements that have a useful life beyond one year on their tax return.