How do you handle errors in accounting?

The best way to correct errors in accounting is to add a correcting entry. A correcting entry is a journal entry used to correct a previous mistake. The type of correcting entry depends on: GAAP (generally accepted accounting practices) guidelines.

How do accountants correct errors found immediately?

Accountants must make correcting entries when they find errors. There are two ways to make correcting entries: reverse the incorrect entry and then use a second journal entry to record the transaction correctly, or make a single journal entry that, when combined with the original but incorrect entry, fixes the error.

What are some examples of counterbalancing errors?

An example of a counterbalancing error is expenses charged to year X that should have been charged to year Y. The result is year X has an overstated expense and an understated profit and year Y has an expense understated and the profit overstated.

As soon as you spot an error, you should correct it in order to make sure your financial statements are accurate. The best way to correct errors in accounting is to add a correcting entry. A correcting entry is a journal entry used to correct a previous mistake.

How do you correct an error of original entry in accounting?

To adjust an entry, find the difference between the correct amount and the error posted in your books. Enter the difference (adjustment amount) in the correct account(s). If the original entry was too low, increase an account. If the original entry was too high, decrease an account.

When accounting errors must be corrected?

Prior Period Errors must be corrected Retrospectively in the financial statements. Retrospective application means that the correction affects only prior period comparative figures. Current period amounts are unaffected. Therefore, comparative amounts of each prior period presented which contain errors are restated.

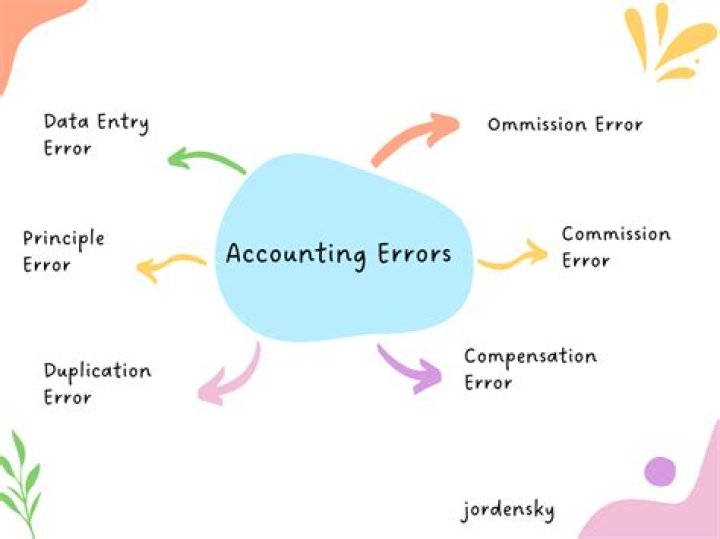

What are the errors of accounting?

Accounting errors can include duplicating the same entry, or an account is recorded correctly but to the wrong customer or vendor. An error of omission involves no entry being recorded despite a transaction occurring for the period.

What is an error of original entry in accounting?

An error of original entry is when the wrong amount is posted to an account. The error posted for the wrong amount would also be reflected in any of the other accounts related to the transaction. In other words, all of the accounts involved would be in balance but for the wrong amounts.

Which of the following is an error of original entry?

An error of original entry occurs when an incorrect amount is posted to the correct account. A particular example of an error of original entry is a transposition error where the numbers are not entered in the correct order.

What do you do when you make an accounting error?

Adding a journal entry may be enough to correct an accounting error. This type of journal entry is called a “correcting entry.” Correcting entries adjust an accounting period’s retained earnings i.e. your profit minus expenses. Correcting entries are part of the accrual accounting system, which uses double-entry bookkeeping.

How does a journal entry correct an accounting error?

Often, adding a journal entry (known as a “correcting entry”) will fix an accounting error. The journal entry adjusts the retained earnings (profit minus expenses) for a certain accounting period. Correcting entries are part of the accrual accounting system, which uses double-entry bookkeeping.

When to make correcting entries in accounting for your business?

A correcting entry in accounting fixes a mistake posted in your books. For example, you might enter the wrong amount for a transaction or post an entry in the wrong account. You must make correcting journal entries as soon as you find an error. Correcting entries ensure that your financial records are accurate.

How is an accounting error corrected under GAAP?

How you correct the error under GAAP depends on the type of error, the number of financial periods the error affects, how the error affects financial statement presentation, and whether the error is counterbalancing.