How do you record gain on marketable securities?

If marketable securities are sold for a price that is higher than their cost, the difference represents a gain on sale of marketable securities. When securities are sold at a gain, cash account is debited, marketable securities account and gain on sale of investment account are credited.

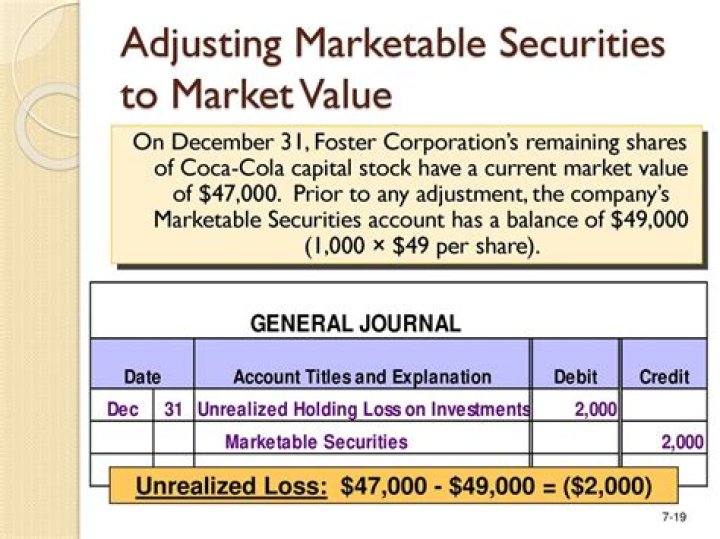

What is the journal entry for unrealized gain?

The accounting for this type of unrealized gain is to debit the asset account Available-for-Sale Securities and credit the Accumulated Other Comprehensive Income account in the general ledger.

Does change in value of marketable securities affect net income?

As the result, the unrealized gain (loss) affects current accounting period and is reported in the income statement. Only the changes in the fair value of trading securities are reported on the income statement in the current period (i.e., affect net income).

How are unrealized gains recorded on a financial statement?

Unrealized gains are recorded on the financial statements differently depending on the type of security, whether they are held-for-trading, held-to-maturity, or available-for-sale. Gains do not affect taxes until the investment is sold and a realized gain is recognized.

What is the definition of a recognized gain?

A recognized gain is when an investment or asset is sold for an amount that is greater than what was originally paid.

When is a sale not a recognized gain?

For example, the sale of a primary residence might not be taxed as a recognized gain if the profit from that sale falls within the guidelines set by the IRS. Thresholds can differ between single tax filers and married filers.

What is the definition of an unrealized gain?

Reviewed by Alicia Tuovila. Updated Aug 9, 2019. An unrealized gain is a potential profit that exists on paper, resulting from an investment. It is an increase in the value of an asset that has yet to be sold for cash, such as a stock position that has increased in value but still remains open.