How do you write a production cost report?

(Steps Enumerated in the Production Report) 1: Analyze the physical flow of production units. 2: Calculate equivalent units for each manufacturing cost element. 3: Determine total costs for each manufacturing cost element. 4: Compute cost per equivalent unit for each manufacturing cost element.

How do you find the total cost of production?

Production costs can include a variety of expenses, such as labor, raw materials, consumable manufacturing supplies, and general overhead. Total product costs can be determined by adding together the total direct materials and labor costs as well as the total manufacturing overhead costs.

How is a production cost report prepared for the first department?

There are four steps in preparing a production cost report. The first step is to summarize the flow of physical units. The next step is to compute output in terms of equivalent units of production. The third step is to compute the cost per equivalent unit of production.

What is the significance of calculating the cost of production?

The accuracy of the calculation of the cost of production is very important because it is useful for companies in making decisions. Errors made in the calculation of cost of goods sold can affect the company’s sales and periodic profits.

What is a production cost report?

The production cost report. summarizes the production and cost activity within a department for a reporting period. It is simply a formal summary of the four steps performed to assign costs to units transferred out and units in ending work-in-process (WIP) inventory.

What is the purpose of a production report?

The production report summarizes the manufacturing activity occurring in a department for a given period. It discloses information concerning the physical flow of units, equivalent units, unit costs, and disposition of manufacturing costs associated with the period.

What is the importance of preparing a production report?

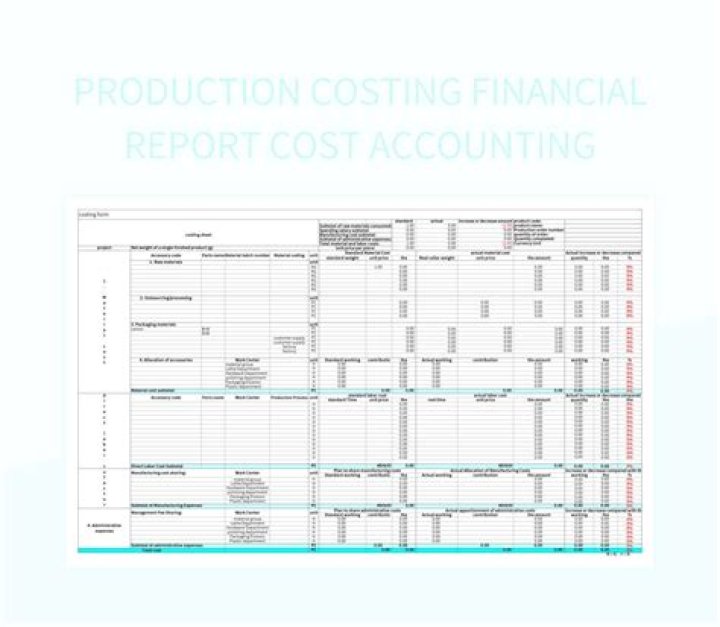

Production cost report : It provides information regarding input units, opening inventory balance, completed units, transferred units, equivalent units, cost per equivalent units, cost of production of units produced and units sold out, and cost of ending inventory.

A cost of production report is prepared using the following four steps:

- Determine the units to be assigned costs.

- Compute equivalent units of production.

- Determine the cost per equivalent unit.

- Allocate costs to units transferred out and partially completed units.

What is total production cost?

Production costs refer to the costs a company incurs from manufacturing a product or providing a service that generates revenue for the company. Total product costs can be determined by adding together the total direct materials and labor costs as well as the total manufacturing overhead costs.

What are the components of the production cost report?

It includes total per unit cost (i.e., total cost incurred divided by total output) as well as per unit cost for individual cost elements like direct materials, direct labor, and manufacturing overhead. The highest production cost among materials, labor and manufacturing overhead.

What is the purpose of a production cost report?

Learning Objective The production cost report. summarizes the production and cost activity within a department for a reporting period. It is simply a formal summary of the four steps performed to assign costs to units transferred out and units in ending work-in-process (WIP) inventory.

How are costs accounted for in production cost report?

In the production cost report, the total A. costs accounted for equals the costs of the units started into production. B. physical units accounted for equals the costs accounted for. C. costs charged equals the units to be accounted for. D. physical units accounted for equals the units to be accounted for.

How are costs charged and physical units accounted for?

C. costs charged equals the units to be accounted for. D. physical units accounted for equals the units to be accounted for. D. physical units accounted for equals the units to be accounted for. THIS SET IS OFTEN IN FOLDERS WITH…

How are unit costs computed in process cost systems?

B. Unit costs are not computed in process cost systems. C. In process cost systems, costs are summarized on job cost sheets. D. In process cost systems, costs are accumulated but not assigned. A.

Which is a true statement about process cost systems?

Which of the following is a true statement about process cost systems? A. A process cost system has one work in process account for each process. B. Unit costs are not computed in process cost systems. C. In process cost systems, costs are summarized on job cost sheets. D. In process cost systems, costs are accumulated but not assigned.