How does an HRA work with an HSA?

The HRA reimburses all deductible expenses above $1,500. You’re eligible to fund an HSA since your HRA is now an HSA-qualified medical plan as well. You can use HSA funds to reimburse the first $1,500 of deductible expenses tax-free before the HRA begins to reimburse your claims.

How do you read an HSA account?

A health savings account, or HSA, is an interest-earning account you can use to help pay for your medical expenses. HSAs provide some tax advantages, but are only an option with certain high-deductible health insurance plans. An HSA is held in a bank or other financial institution.

How is an HRA different from HSA?

An HRA is an arrangement between an employer and an employee allowing employees to get reimbursed for their medical expenses, while an HSA is a portable account that the employee owns and keeps with them even after they leave the organization.

Can you have HSA and HRA at same time?

The answer is yes. Under specific circumstances, you can have an HRA and HSA at the same time. Employers must also ensure their HRAs are HSA eligible before employees can utilize both accounts.

Can I have an HSA if my husband has an HRA?

Even though you are not covered by your spouse’s health insurance, the IRS considers your spouse’s Healthcare FSA or HRA to be “other insurance.” If your spouse participates in either an HSA-Compatible FSA or a limited-purpose HRA, then yes, you may participate in an HSA.

How much should I put in my HSA?

Here are some key guidelines for determining how much to contribute to an HSA: As an individual, you can put up to $3,550 an HSA in 2020. Those with a family HSA have a contribution limit of $7,100. If you are 55 or older, you can put an additional $1,000 in an HSA.

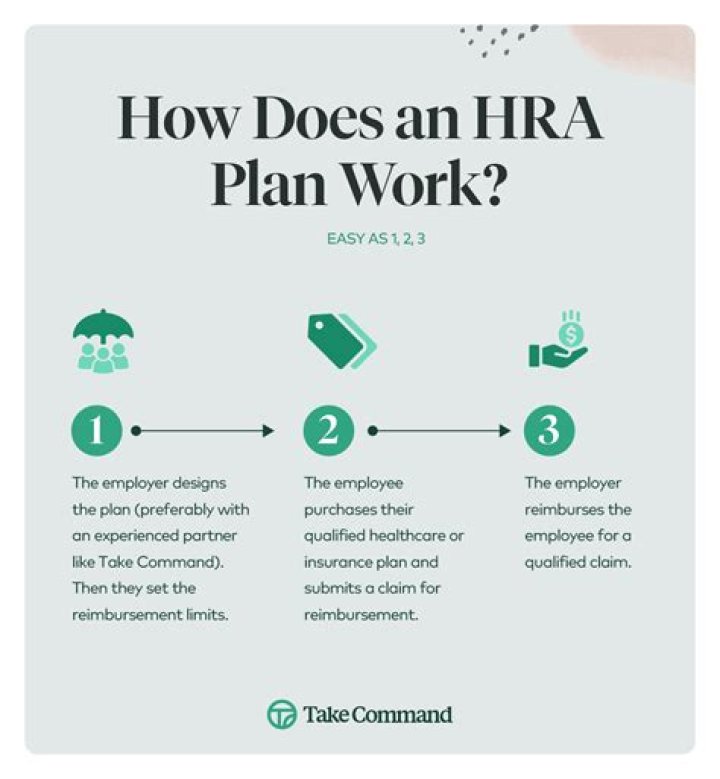

Is an HRA worth it?

A Health Reimbursement Arrangement (HRA), can be one of the most effective ways to save money on your group health insurance premiums. In fact, some companies can save upwards of 30% over traditional plan setups.

How much can I contribute to my HSA in 2020?

$3,550

Consumers can contribute up to the annual maximum amount as determined by the IRS. Maximum contribution amounts for 2020 are $3,550 for self-only and $7,100 for families. The annual “catch- up” contribution amount for individuals age 55 or older will remain $1,000.

What can I spend my HSA on?

In general, you can use your HSA to pay for any qualified medical expense. Qualified medical expenses are defined by the IRS and include medical care, vision and dental care expenses, prescription drugs, and payments for long term care services and insurance.

Yes. If the HRA meets the requirements for an HSA-qualified medical plan and you satisfy all other eligibility requirements, you can open and fund to an HSA and receive employer reimbursement funds tax-free through an HRA. You’re eligible to fund an HSA since your HRA is now an HSA-qualified medical plan as well.

How does an HRA differ from an HSA?

Are HRA Plans good?

Why do I need a HRA and an HSA?

Healthcare spending accounts, such as Health Reimbursement Arrangements (HRAs) and Health Savings Accounts (HSAs), help individuals and families pay for medical expenses. They also provide more control over how and where to pay for those expenses.

What can you do with an HSA account?

An HSA acts like a long-term savings account you can use to pay for qualified health care expenses. You deposit pre-tax money from each paycheck into the account, and then make withdrawals to pay for eligible medical expenses as needed. Your employer can also contribute to the account, but is not required to.

Can a HRA account be used for rollover?

First, the HRA account is owned by and funded only by the employer. The employer deposits a predetermined amount of money into the account which you can then use to pay for medical expenses not covered by your health plan. HRA funds may be eligible for rollover (depending on your plan), but cannot be invested.

Can a HRA be opened to all employees?

Individual HRAs may be open to all employees, or your employer might only offer them to certain classes of employees, like salaried employees but not hourly workers. An HSA can be opened through an employer or on your own. Whether you open an HSA through work or independently, the same eligibility requirements stand.