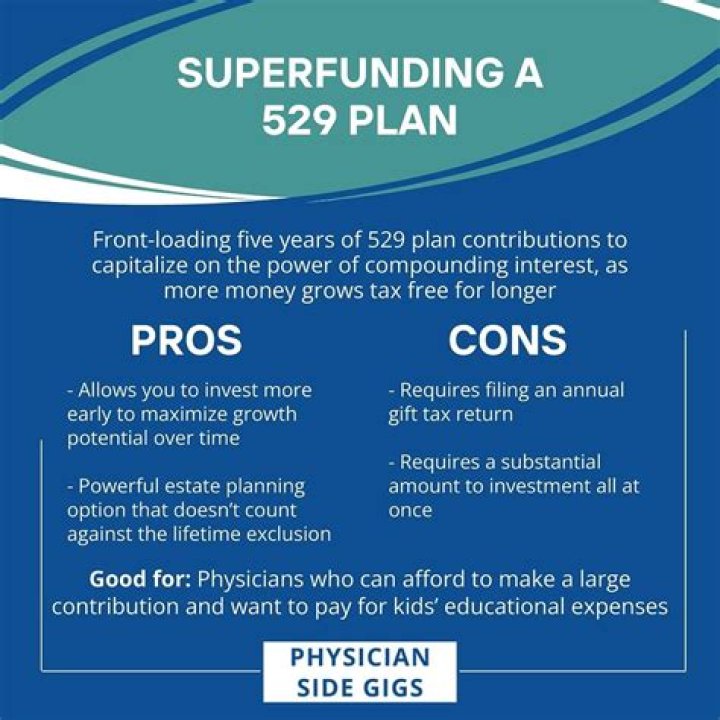

How does Superfunding a 529 work?

Superfunding, or 5-year gift-tax averaging, allows families to front-load large contributions to a 529 plan without having to pay gift taxes, while protecting their lifetime gift and estate tax exemption. The annual gift tax exclusion amount is $15,000 per donor per beneficiary in 2019.

Are withdrawals from 529 plans taxable?

529 withdrawals are tax-free to the extent your child (or other account beneficiary) incurs qualified education expenses (QHEE) during the year. If you withdraw more than the QHEE, the excess is a non-qualified distribution. The principal portion of your 529 withdrawal is not subject to tax or penalty.

What is Superfunding a 529 plan?

“Superfunding” is a term sometimes used to describe large 529 plan contributions using 5-year gift tax averaging described in section 529(c)(2)(B) of the Internal Revenue Code. Superfunding their 529 plan accounts would reduce their estate by $1.5 million in a single day without using any of their lifetime exemptions.

What happens if you Superfund a 529 plan?

Superfunding their 529 plan accounts would reduce their estate by $1.5 million in a single day without using any of their lifetime exemptions. Tax law allows 5-year gift tax averaging only for gifting that involves 529 plans (and in rare situations, Coverdell education savings accounts).

Is there a 5 year gift tax on 529 plans?

Tax law allows 5-year gift tax averaging only for gifting that involves 529 plans (and in rare situations, Coverdell education savings accounts). Here are a few rules and tips to keep in mind when considering superfunding a 529 plan.

Is it possible to fully fund a 529 plan?

It is based on what the state believes is the full cost of attending an expensive college and graduate school. This amount is including textbooks and room and board. However, it is possible to fully fund a 529 plan account without having to pay gift taxes.

What’s the maximum contribution to a 529 plan?

Individuals are not subject to gift tax or generation-skipping transfer tax (GST) unless the total amount of cash and properties they give away over the course of their lifetime exceeds $11.58 million for 2020. 529 plan aggregate contribution limits range from $235,000 to $529,000, depending on the state.