How is Qbi 2020 calculated?

In the case of a non-SSTB, when taxable income exceeds the threshold amount, the QBI deduction is calculated by taking the lesser of:

- 20% of QBI; or.

- The greater of: 50% of the W-2 wages; or. The sum of 25% of the W-2 wages plus 2.5% of the UBIA of all qualified property.

Who should use Form 8995?

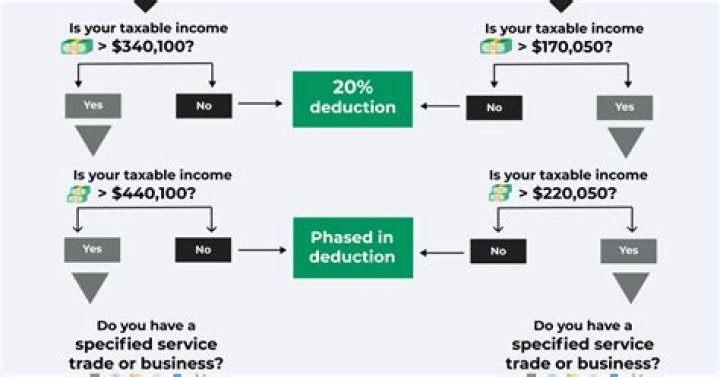

If your work qualifies you for certain business deductions on your taxes, you may need to use Form 8995. The pass-through deduction, also known as the Qualified Business Income Deduction, allows owners of pass-through businesses to deduct up to 20% of their share of qualified business income.

How does the qualified business income ( QBI ) deduction work?

The QBI deduction is a personal write-off that you can claim whether you take the standard deduction or itemize personal deductions. The QBI deduction does not reduce business income or have any impact on self-employment tax for owners who are treated as self-employed individuals. 2. What counts as qualified business income (QBI)?

Are there any new tax breaks for qualified business income?

One of the more important provisions in the Tax Cuts and Jobs Act, passed in December of 2017, is the new Section 199A – the deduction for qualified business income (QBI). Section 199A allows a deduction for up to 20% of QBI from partnerships, limited liability companies (LLCs), S corporations, trusts, estates, and sole proprietorships.

What makes up 20 percent of qualified business income?

20 percent of the taxpayer’s qualified business income (QBI), plus 20 percent of the taxpayer’s qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income, or 20 percent of the taxpayer’s taxable income minus any net capital gains.

What are the limitations on qualified business income?

These limitations include: the type of trade or business; the taxpayer’s taxable income; and the amount of W-2 wages paid by the qualified business. Another limitation to the deduction is caused by what is known as the unadjusted basis immediately after acquisition (or UBIA) of qualified property held by the trade or business.