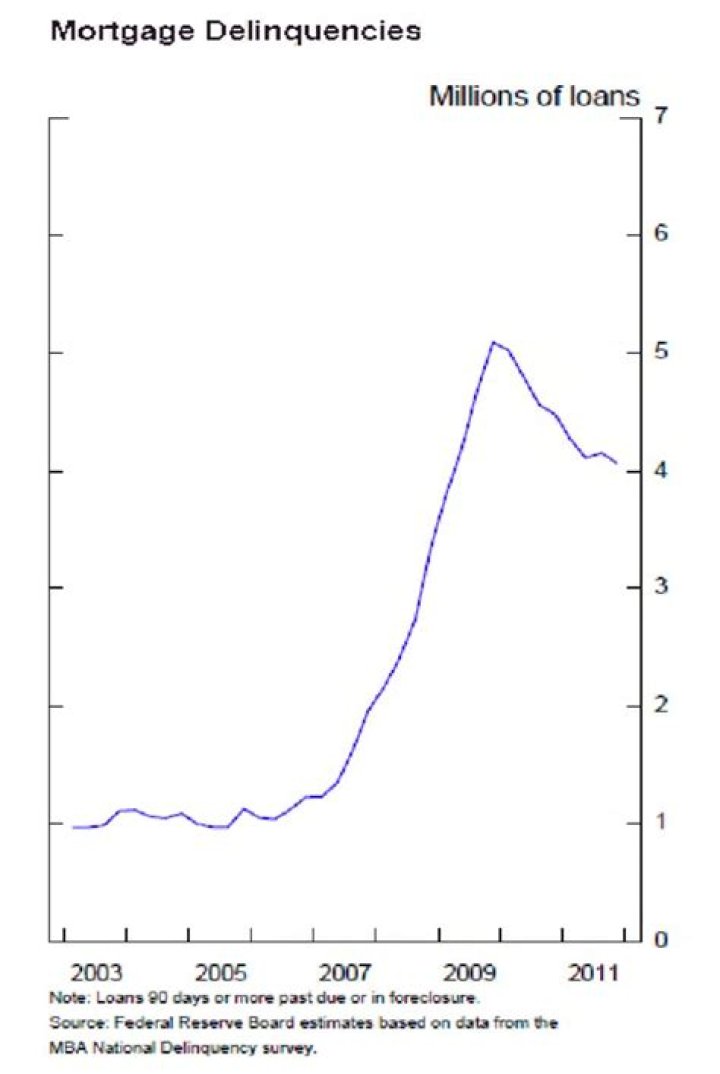

How many mortgages defaulted 2008?

This increased to 2.3 million in 2008, an 81% increase vs. 2007, and again to 2.8 million in 2009, a 21% increase vs. 2008. By August 2008, 9.2% of all U.S. mortgages outstanding were either delinquent or in foreclosure.

What happened in the 2008 mortgage crisis?

Hedge funds, banks, and insurance companies caused the subprime mortgage crisis. Demand for mortgages led to an asset bubble in housing. When the Federal Reserve raised the federal funds rate, it sent adjustable mortgage interest rates skyrocketing. As a result, home prices plummeted, and borrowers defaulted.

Why did home prices fall in 2008?

The 2007–08 Housing Market Crash Low interest rates, relaxed lending standards—including extremely low down payment requirements—allowed people who would otherwise never have been able to purchase a home to become homeowners. This drove home prices up even more. This, in turn, caused prices to drop.

What was the first time home buyer tax credit for 2008?

Repaying the 2008 First-Time Home Buyer Tax Credit. If you were a first-time home buyer between April 8, 2008 and January 1, 2009, you might recall taking advantage of The Housing and Economic Recovery Act of 2008 that allowed eligible homeowners to utilize an interest-free loan equal to 10% of the purchase price of a home (up to $7,500).

Why was the first time Home Buyer credit created?

The First-Time Homebuyer creditwas an incentive by Congress to boost housing sales in a time when the Great Recession made it difficult to purchase a home. Those who took advantage of the credit are required to repay the government in equal installments over 15 years for the amount received.

How to get a home purchase loan closed?

Get your refinance or home purchase loan closed timely and smoothly. Because A Local Approach is Better! Answer a few simple, quick questions. Get a no obligation rate quote and loan options.

What was the percentage of subprime mortgages in 2006?

A high percentage of these subprime mortgages, over 90% in 2006 for example, were adjustable-rate mortgages. Housing speculation also increased, with the share of mortgage originations to investors (i.e. those owning homes other than primary residences) rising significantly from around 20% in 2000 to around 35% in 2006–2007.