How many years can loss be allowed a carryback?

5 years

New rules for NOL carrybacks. Section 2303 of the CARES Act amended section 172 as revised by the Tax Cuts and Jobs Act (TCJA), section 13302, for tax years 2018, 2019, and 2020. Taxpayers can carry back NOLs, including non-farm NOLs, arising from tax years beginning in 2018, 2019, and 2020 for 5 years.

Can you carry back trading losses against capital gains?

Only if there is insufficient other income to absorb the trading loss can the excess trading loss element be offset against capital gains of the tax year. In the event that there are still unrelieved trading losses, these may be carried back to the previous tax year for offset in the same manner.

Most taxpayers no longer have the option to carryback a net operating loss (NOL). For most taxpayers, NOLs arising in tax years ending after 2020 can only be carried forward. The 2-year carryback rule in effect before 2018, generally, does not apply to NOLs arising in tax years ending after December 31, 2017.

Can individuals carryback losses?

Under the TCJA rules, businesses couldn’t carry back NOLs. Under the CARES Act, an NOL from a tax year beginning in 2018, 2019 or 2020 can be carried back five years. Taxpayers don’t have to carryback their 2018, 2019 and 2020 NOLs.

When does a corporation have a tax loss carryback?

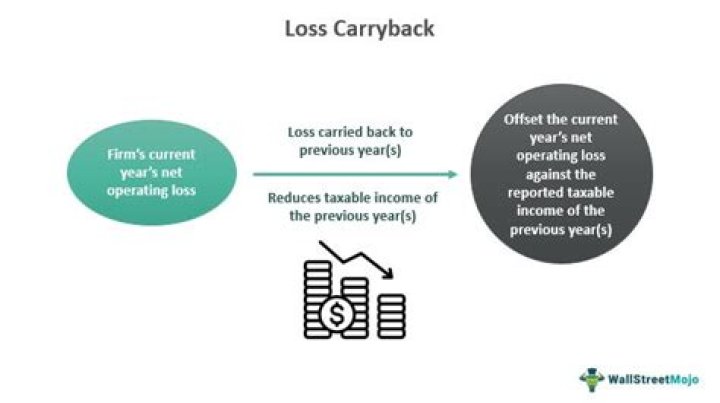

Tax loss carryback. Tax loss carryback is when NOL year net operating loss is set off against taxable income in past periods. In US, tax loss carryback is optional i.e. a corporation may waive its right to carryback NOL and instead may opt to just carryforward the losses. Tax loss carryback results in recognition of income tax refund receivable.

When do you have to carry back a net operating loss?

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) amended section 172 (b) (1) to provide for a carryback of any net operating loss (NOL) arising in a taxable year beginning after December 31, 2017, and before January 1, 2021, to each of the five taxable years preceding the taxable year in which the loss arises (carryback period).

What is an example of tax loss carryforward?

Tax loss carryforward results in recognition of a deferred tax asset. Let’s continue with our example above. $25 million of net operating loss related to 2017 couldn’t be carried back because the corporation ran out of available taxable income. The remainder of the NOL which can’t be carried back can be carried back for 20 years.

When to exclude 965 years from carryback period?

After April 9, 2020, you may make the election to exclude all section 965 years from the carryback period by attaching an election statement to the earliest filed of the following: The Federal income tax return for the taxable year in which the NOL arises,