How should assets be recorded?

Assets are recorded at their cost and (except for some securities) are not adjusted for changes in market value. Long-term assets such as buildings and equipment are depreciated and therefore will be reported at less than their cost.

Is impairment the same as write-down?

A write down is necessary if the fair market value (FMV) of an asset is less than the carrying value currently on the books. The income statement will include an impairment loss, reducing net income. An impairment can not be deducted on taxes until the asset is sold or disposed.

Assets are recorded at their cost and (except for some securities) are not adjusted for changes in market value. Assets are part of the accounting equation and the balance sheet, both of which are presented in this format: Assets = Liabilities + Stockholders’ (or Owner’s) Equity.

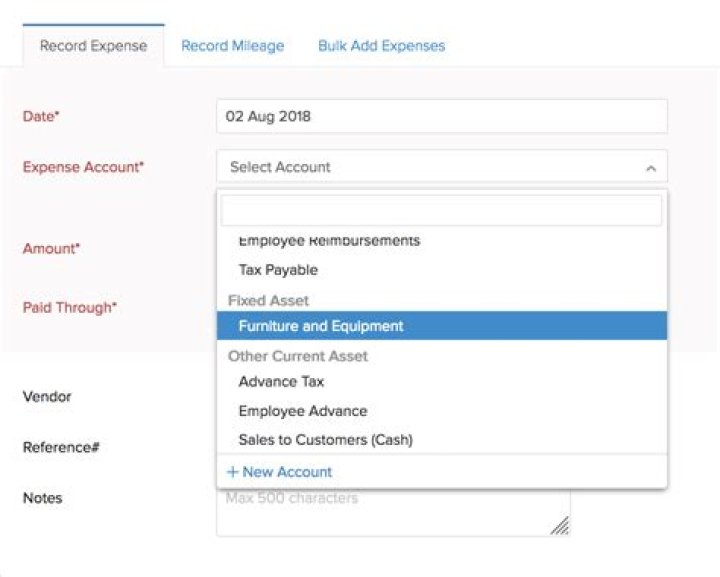

What are the different methods of recording assets?

The easiest, most accurate way to manage and record your assets is by using accounting software, but even if you’re using a manual accounting system, assets will still need to be managed properly….6 types of assets

- Cash accounts.

- Cash equivalent accounts.

- Accounts receivable.

- Inventory.

When do you need a business asset record?

Capital losses that occur when your business sells an asset for less than its investment in it can result in a business tax credit. Your asset records are crucial in both situations, establishing your investment and detailing the sales transaction. When in doubt, hang onto that paperwork.

How does a business record the disposal of an asset?

Recording the disposal of an asset requires taking several steps. First, the business must ensure that the asset’s depreciation account is up to date. Then the business must write off the asset balance as well as its accumulated depreciation balance. Then it must record any cash or property it received in exchange for the asset.

Where do you record business transactions in accounting?

A journal, which is also known as a book of original entry, is the first place that a transaction is written in accounting records. Even when you’re using a computerized accounting program, items are still recorded in journals; you just don’t manually enter them. The best way to learn how to record business transactions is to actually record some.

Why is it important to keep asset Records?

Keeping complete and accurate asset records can save you money — not to mention headaches — at tax time. Your business’s assets contribute to its value, and your asset records can play a critical role at tax time.