In which situations is a 1099 NEC not required to be issued?

1. The payment is $600 or more for services — not physical products. The first rule of thumb is that the payment must be at least $600. If it’s less than that amount, a 1099-NEC is not required and should not be issued.

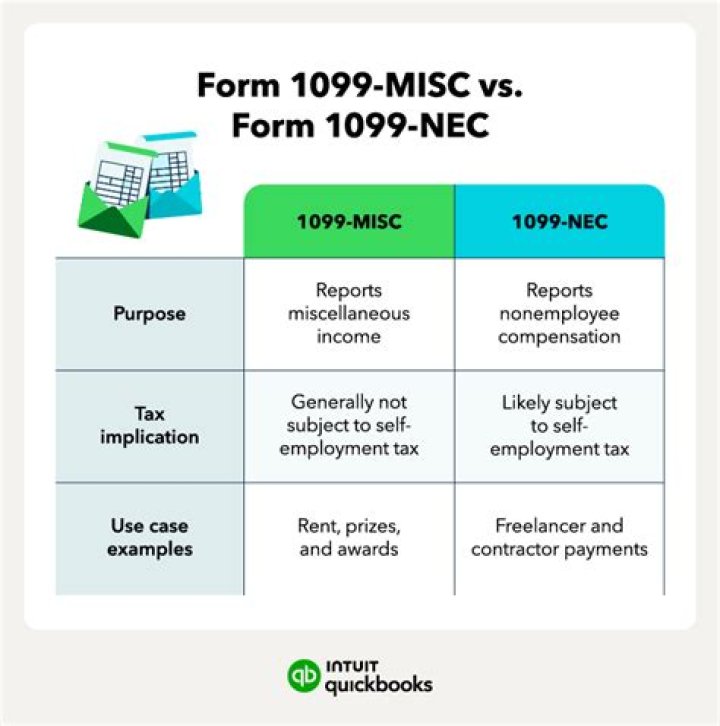

Who files a 1099-NEC?

Who needs to file Form 1099-NEC? Any business that makes nonemployee compensation payments totaling $600 or more to at least one payee or withholds federal income tax from a nonemployee’s payment, will now use this revamped form to report those payments and withholding.

What do you need to know about a 1099-R tax form?

A 1099-R is an IRS tax form that reports distributions from annuities, IRAs, retirement plans, profit-sharing plans, pensions, and insurance contracts. The gross amount of the distribution, taxable amount, employee contributions, tax withholding, and the distribution code are reported to the contract owner and the IRS.

Can a 1099-R be received if no money is withdrawn?

A: For qualified contracts, such as IRAs, distributions are 100% taxable. For nonqualified contracts, any earnings above the cost basis are taxable. For more information about cost basis, click here. Q: Can a 1099-R be received even if no money was withdrawn during the tax year? A: Yes, a 1099-R can still be received.

Are there any exceptions to the 1099 distribution code?

1099-R Distribution Code Exceptions Most retirement plan distributions reported on Form 1099-R and paid to the client before age 59 ½ are subject to an additional tax of 10% (often referred to as an early withdrawal “penalty,” though it is not a penalty by definition).

Where is the 1099-R sent to the contract owner?

If applicable, a 1099-R is mailed to the contract owner’s address of record. For clients enrolled in electronic delivery, notification of 1099-R availability on the website is sent to the email address on record. The information on the 1099-R is based on the contract owner, not the annuitant (except for 457(b)…