Is a Roth IRA conversion taxable distribution?

Roth conversions and RMDs RMD amounts cannot be included in the converted amount. The amount you choose to convert will be taxed as ordinary income. The total taxable amount is affected by whether the underlying contributions to the IRA were deductible.

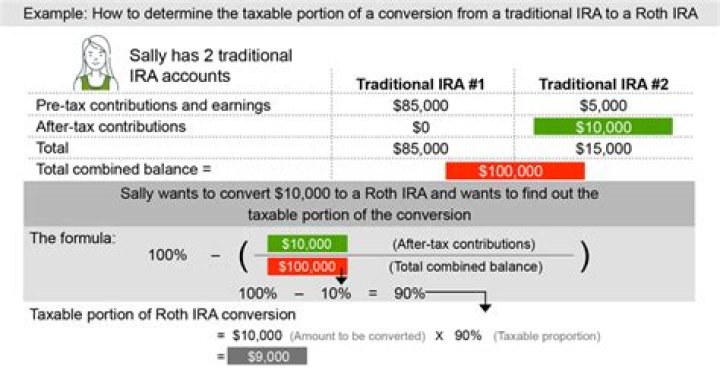

Under current law, qualified distributions from Roth IRAs are not included when determining the taxable portion of your Social Security. The assets you convert are subject to federal and possibly state income tax for the year you convert (to the extent that the converted amount represents pre-tax assets).

Do you have to pay taxes on early withdrawal from Roth IRA?

If you want to withdraw earnings: You must satisfy two requirements for a qualified distribution to avoid both taxes and the 10% early withdrawal penalty. First, you must have held a Roth IRA account for at least five years, a clock that starts ticking at the beginning of the year of your first contribution.

Is the distribution from a Roth IRA taxable?

This interview will help you determine if your distribution from a Roth IRA or designated Roth account is taxable. This topic doesn’t address either the return of a Roth IRA contribution or return of a prior year’s excess contribution, or a corrective distribution of excess contribution from a designated Roth account.

How old do you have to be to take distributions from a Roth IRA?

If you’ve held your Roth IRA for at least five years and you’re older than age 59 1/2, money you withdraw will be tax-free. If you open a Roth IRA account after you turn 59 1/2, you still have to wait at least five years before you can take distributions of your earnings without an early withdrawal penalty.

What is the tax code for a Roth IRA?

When you are entering this information into TurboTax, your Form 1099-R, box 7 codes J, Q and T identifies a Roth IRA distribution and determines the tax treatment. If you have a J or a Q, the distribution is considered taxable unless there is an exception.