Is beta correlation or covariance?

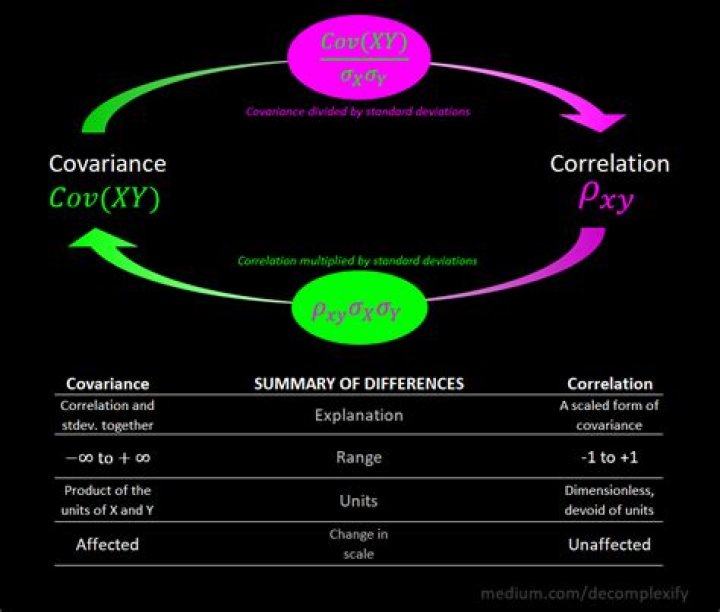

Covariance is used to measure the correlation in price moves of two different stocks. The formula for calculating beta is the covariance of the return of an asset with the return of the benchmark, divided by the variance of the return of the benchmark over a certain period.

Why is beta of market Portfolio 1?

A beta between 0 and 1 signifies that it moves in the same direction as the market, but with less volatility—that is, smaller percentage changes—than the market as a whole. A beta of 1 indicates that the portfolio will move in the same direction, have the same volatility and is sensitive to systematic risk.

What does the beta of a stock measure?

Beta is a measure of a stock’s volatility in relation to the overall market. By definition, the market, such as the S&P 500 Index, has a beta of 1.0, and individual stocks are ranked according to how much they deviate from the market. If a stock moves less than the market, the stock’s beta is less than 1.0.

How do you analyze beta of a stock?

The beta coefficient is calculated by dividing the covariance of the stock return versus the market return by the variance of the market. Beta is used in the calculation of the capital asset pricing model (CAPM). This model calculates the required return for an asset versus its risk.

Is beta same as correlation?

The beta measure incorporates the correlation and the relative risk, making it a more useful measure of relative investment behaviour. In modern portfolio theory, an efficient portfolio is one that combines individual investments in such a way as to maximize the expected rate of return for a given level of risk.

Is the beta of the market always 1?

The beta of market portfolio is always one. Because beta measures the sensitivity of an asset to the movements of the overall market portfolio, and the market portfolio obviously moves precisely with itself, its beta is one.

What is the difference between R and beta?

R-squared measures how closely each change in the price of an asset is correlated to a benchmark. Beta measures how large those price changes are in relation to a benchmark.

What is the disadvantage of beta?

The largest drawback of using Beta is that it relies solely on past returns and does not account for new information that may impact returns in the future. Furthermore, as more return data is gathered over time, the measure of Beta changes, and subsequently, so does the cost of equity.

Why is beta of Market Portfolio 1?

Beta is a measure of a stock’s volatility in relation to the overall market. If a stock moves less than the market, the stock’s beta is less than 1.0. High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

What has a beta of 1?

Beta of 1: A beta of 1 means a stock mirrors the volatility of whatever index is used to represent the overall market. If a stock has a beta of 1, it will move in the same direction as the index, by about the same amount.

How to calculate the beta of the stock market?

The formula for the beta can be written as: Beta = Covariance stock versus market returns / Variance of the Stock Market See above for calculation of covariance. You may also see Beta expressed as the following formula:

How are beta and covariance related to stock returns?

So, it would seem that beta and covariance are linked in some way since they are so similar. Indeed they are. Think about it, if the covariance is high, the stocks move in sync and positively, then beta must be higher.

What kind of stocks have a lower beta?

Many consider stocks in the utility sector to have betas less than 1 since they’re not very volatile. Gold, on the other hand, is quite volatile but has at times had a tendency to move inversely to the market. Lower beta stocks with less volatility do not carry as much risk, but generally provide less opportunity for a higher return.

What is the beta of NASDAQ stock XYZ?

XYZ has a standard deviation of returns of 22.12%, and NASDAQ has a standard deviation of returns of 22.21%. Use the following data for the calculation of the beta.