Is cash received in a merger taxable?

The merger qualifies as a “tax-free reorganization” under the tax law. That’s usually the case if at least half the consideration you receive is in the form of stock. The only consideration you receive in addition to common stock of the acquiring company is cash.

What happens to your money when a stock merges?

After a merge officially takes effect, the stock price of the newly-formed entity usually exceeds the value of each underlying company during its pre-merge stage. In the absence of unfavorable economic conditions, shareholders of the merged company usually experience favorable long-term performance and dividends.

Are stock swaps taxed?

Swapping shares is generally a non-taxable event. However, the exercise itself is a taxable event subject to normal NQSO tax rules. This means that the bargain element of your exercised non-qualified stock options is subject to ordinary income, Medicare, and Social Security tax, if applicable.

What are the tax consequences of a merger?

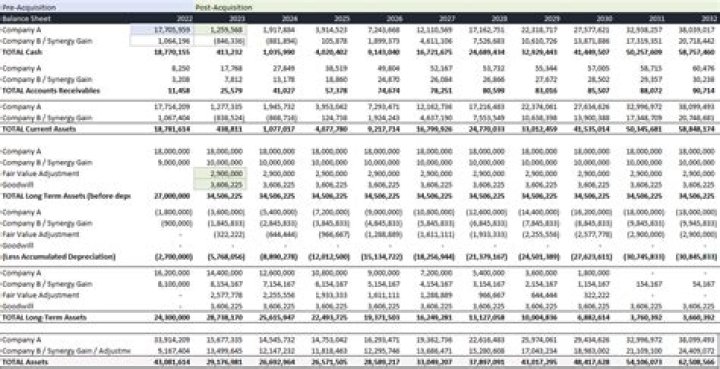

For instance, if Company A merges with Company B, Company A will pay taxes on assets and taxes acquired while Company B pays no taxes, assuming the immediate liquidation of B. If B survives, it must declare income earned through the sale of stock or assets and pay taxes on this capital if the amount exceeds all losses.

How does a stock and cash merger work?

Since you can’t recognize a loss you set your basis against whatever “proceeds” the broker is reporting, which might be only the cash or might be the combination of cash plus stock, to the same amount as the proceeds, reporting no gain or loss.

How to report a stock sale after a merger?

The 1099-B lists the proceeds of the sale, and it is then up to you to compute the proper capital gain or loss. Download Schedule D from the IRS website if you have a capital gain or loss to report.

How does exchange ratio work in all stock mergers?

In an “all stock” merger, the exchange ratio can result in a fraction of a share being owed to the owner of stock in the acquired company. Rather than issue a portion of a share, the investor is paid “cash in lieu” of a fractional share. These payments are always small and less than the market value of one share.

How to calculate cost basis after a merger?

Subtract the result in the previous step from the total number of shares of the original acquired company stock you own, then multiply by your original cost basis per share, to get the cost basis for the cash portion of the merger.