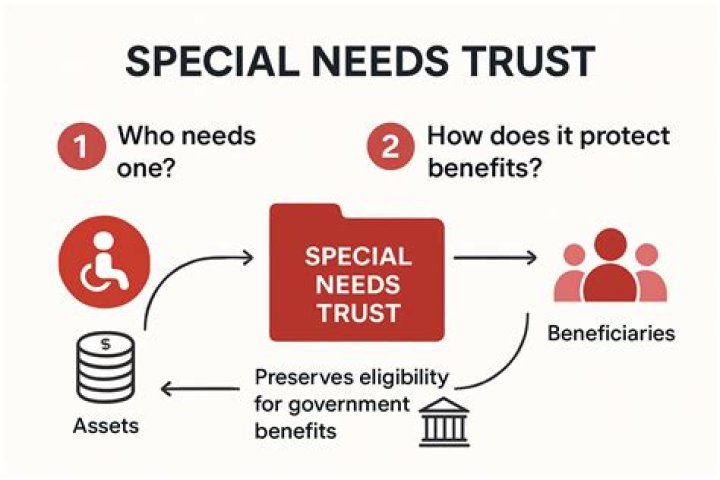

Is income from a special needs trust taxable?

If a third-party SNT is considered a grantor trust, all items of income, deduction and credit are generally taxed to the individual(s) who created and funded the SNT (typically parents or other relatives of the beneficiary with a disability). All items of income, deduction and credit are reported on Form 1041.

Are distributions from a special needs trust taxable to the beneficiary?

Most special needs trusts are third party special needs trusts, and they are taxed as a pass-through entity. From that amount, the trust may deduct any distributions that were made to the beneficiary. So the trust does not pay taxes on any income that it earns as long as that income is passed on to the beneficiary.

Can a trust receive income?

Principal Distributions. When trust beneficiaries receive distributions from the trust’s principal balance, they do not have to pay taxes on the distribution. Once money is placed into the trust, the interest it accumulates is taxable as income, either to the beneficiary or the trust itself.

Are distributions from a special needs trust taxable to the recipient?

Do you have to file a tax return for a special needs trust?

If the SNT’s income must be reported by the beneficiary on his own personal return, the SNT document should allow the SNT to pay the beneficiary’s income tax liability from the assets in the SNT.

What kind of trust is a special needs trust?

Third-party SNTs are generally considered either “complex trusts” or “qualified disability trusts” for income tax purposes. The SNT itself is responsible for reporting its own items of income, deduction and credit.

What’s the maximum amount SSI can be paid to a special needs trust?

In January, 2019, the maximum SSI benefit was increased to $771 per month. Food and shelter expenses paid for by the special needs trust (or any other source) are considered income as in-kind support and maintenance (ISM) to a third party provider of goods or services.

Can you pay credit card bill with special needs trust?

Purchase of personal items such as clothing, a computer, paying a phone bill or income taxes, would have no impact on SSI. But if food or shelter items are purchased, it is deemed ISM. An example of where this can get confusing is when a special needs trust pays a credit card bill. SI 01120