Is it worth taking the home office deduction?

Small-business owners and entrepreneurs who work from home could save big money on their taxes by taking the home office deduction, as long as they meet the IRS’ requirements and keep good records.

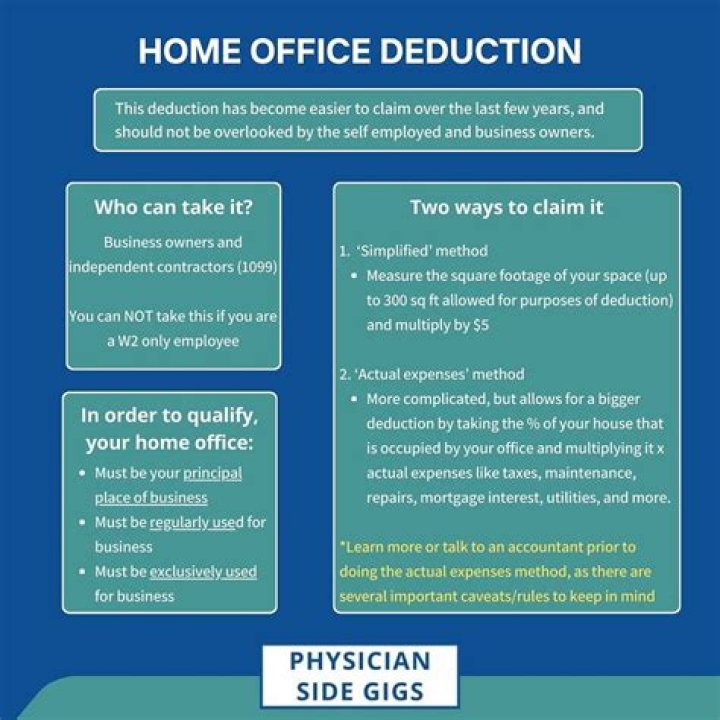

Can I deduct my work from home office?

You can’t take the home office deduction unless you use part of your home exclusively for your business. If you use part of your home—such as a room or studio—as your business office, but you also use that space for personal purposes, you won’t qualify for the home office deduction.

Can I deduct my home office in 2019?

As a result of the TCJA, for the tax years 2018 through 2025, you cannot deduct home office expenses if you are an employee. The TCJA did not change the home office expense rules for self-employed persons. If you are self-employed, you can continue to deduct qualifying home office expenses.

Who is eligible for the Home Office deduction?

Employees are not eligible to claim the home office deduction. The home office deduction Form 8829 is available to both homeowners and renters. There are certain expenses taxpayers can deduct.

Can you deduct home office expenses for business use?

If you use part of your home for business, you may be able to deduct expenses for the business use of your home. If you use part of your home for business, you may be able to deduct expenses for the business use of your home. The home office deduction is available for homeowners and renters, and applies to all types of homes.

Is the Home Office deduction still valid in 2017?

While still a legitimate deduction in 2017, the new tax law removes miscellaneous deductions from the tax return. While the home office deduction, especially for the self-employed, can be of benefit to those who qualify, a great deal of scrutiny must accompany its use.

How does the simplified home office deduction work?

Simplified Option. This new simplified option can significantly reduce the burden of recordkeeping by allowing a qualified taxpayer to multiply a prescribed rate by the allowable square footage of the office in lieu of determining actual expenses.