Is money inherited from a revocable trust taxable?

Someone who inherits money from a revocable trust receives it tax-free, but the estate might have to pay estate tax on everything that it contains before distributing it.

Is an inherited trust revocable?

Living trusts can be revocable or irrevocable and also can help avoid probate. If you have inherited a trust, you may want to consider consulting with an estate attorney or certified tax professional who can guide you through the next steps.

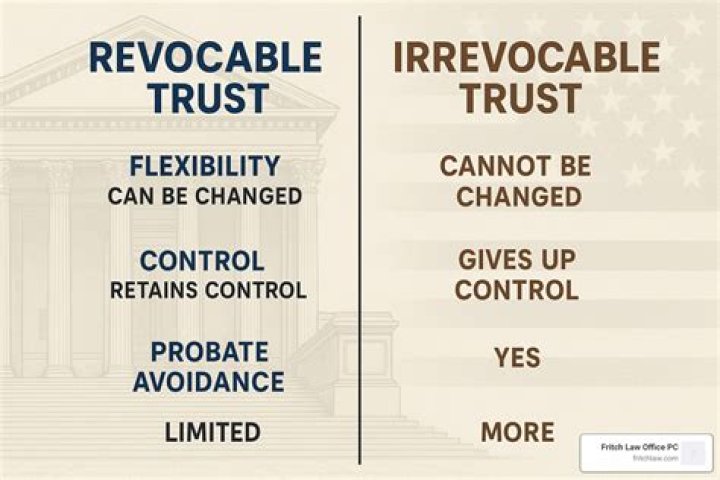

What is revocable trust mean?

A revocable trust typically provides that property be managed for the grantor’s benefit. In most cases, the grantor retains certain rights over the trust during his or her lifetime. When a grantor dies, the trust acts like a will, and the property is distributed to the beneficiaries as directed by the trust agreement.

Can a grandchildren Trust be a generation skipping Trust?

You can also determine if your grandchildren will be able to control the money at a certain age as either co-trustees or full owners. Generation-skipping trusts can allow trust assets to be distributed to non-spouse beneficiaries two or more generations younger than the donor without incurring GST tax.

Do you have to pay inheritance tax on transfer to discretionary trust?

Even if no Inheritance Tax is due on the transfer you may need to add its value to the deceased’s estate when you are working out the value for Inheritance Tax purposes. The additional threshold will not apply to transfers of a home or any other assets to a discretionary trust before a person died.

Who is the grantor of a revocable living trust?

The trust instrument is the document that creates the trust, defines the rights and responsibilities of the parties, and sets the terms of the trust. When someone makes a revocable living trust, they can occupy all three roles: grantor, trustee, and beneficiary.

What happens when a home is held in a discretionary trust?

If the home is held in a discretionary trust, it would not normally be included in the beneficiary’s estate. When the beneficiary dies, their estate will not be eligible for the additional threshold even if the home goes to the beneficiary’s direct descendants. 2. When the deceased transferred assets into a trust before they died