What affects shareholder basis?

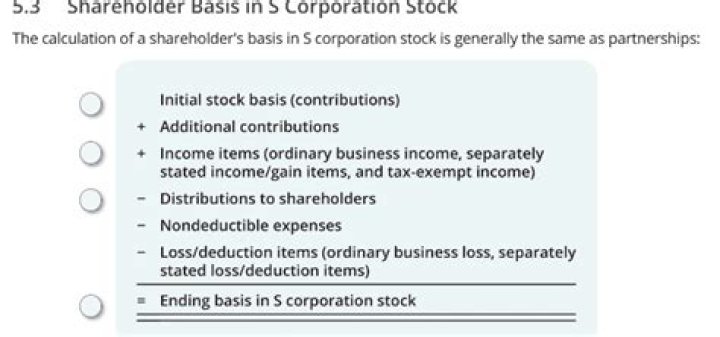

Stock basis is adjusted annually, as of the last day of the S corporation year, in the following order: Increased for income items and excess depletion; Decreased for distributions; Decreased for non-deductible, non-capital expenses and depletion; and.

What does it mean to have basis in a company?

Your basis in a business asset is basically the cost of that asset. The term applies to all kinds of capital assets that are owned by your business, including real estate, land, equipment, and investments owned by the company, such as stocks, bonds, ETF’s, and mutual funds.

What is a basis sheet?

An S corp basis worksheet is used to compute a shareholder’s basis in an S corporation. Shareholders who have ownership in an S corporation must make a point to have a general understanding of basis. According to the IRS, basis is the amount of the shareholder’s investment in the business for tax purposes.

What are the items affecting the shareholder basis?

Items Affecting Shareholder Basis Line 16A – Tax-Exempt Interest Income – This amount represents the taxpayer’s share of tax-exempt interest. This amount will automatically pull to Form 1040, line 2a. Line 16B – Other Tax-Exempt Income – This amount represents the taxpayer’s other tax-exempt income.

What makes a shareholder’s stock increase on a tax return?

A shareholder’s stock is increased by (using 2018 Form 1120S Schedule K-1 box items): 1. Ordinary income 2. Separately stated income items 3. Tax exempt income 4. Excess depletion A shareholder’s stock basis is decreased, but not below zero, by:

How to enter items affecting shareholder’s basis on Form 1120S?

To enter the Items Affecting Shareholder’s Basis from a K-1 (Form 1120S) in TaxSlayer Pro from the Main Menu of the Tax Return (Form 1040) select: K-1 Input and select ‘New’ and double-click on Form 1120S K-1 S Corporation which will take you to the K-1 Heading Information Entry Menu.

Is the stock and debt basis of a corporation taxable?

The taxable amount of a distribution is contingent on the shareholder’s stock basis. It is not the corporation’s responsibility to track a shareholder’s stock and debt basis but rather it is the shareholder’s responsibility.