What are basic principles of economics?

These key principles include scarcity (the basic economic problem that exists because we as humans have unlimited wants that cannot be met by the limited amount of resources our world has), the marginal impact (the impact of a small or one-unit change), incentives (such as prices, taxes, and fees), markets (places …

What is the most important principle of economics?

At the most basic level, economics attempts to explain how and why we make the purchasing choices we do. Four key economic concepts—scarcity, supply and demand, costs and benefits, and incentives—can help explain many decisions that humans make.

What are the principles of how the economy as a whole works?

The three principles that describe how the economy as a whole works are: (1) a country’s standard of living depends on its ability to produce goods and services; (2) prices rise when the government prints too much money; and (3) society faces a short-run tradeoff between inflation and unemployment.

Who is the first mother of India?

Bhikaiji Rustom Cama,or Madam Cama was born on 24 September 1861 in Bombay. She was an outstanding lady of great courage, fearlessness, integrity, perseverance and passion for freedom. and is considered as the mother of Indian revolution because of her contributions to Indian freedom struggle.

What are the principles of economics and policy making?

1. The four principles of economic decisionmaking are: (1) people face tradeoffs; (2) the cost of something is what you give up to get it; (3) rational people think at the margin; and (4) people respond to incentives.

How does the economy as a whole work?

What are the 3 economic principles?

The essence of economics can be reduced to three basic principles: scarcity, efficiency, and sovereignty. These principles were not created by economists. They are basic principles of human behavior. These principles exist regardless of whether individuals live in market economies or planned economies.

What’s the first rule of economics?

“The first lesson of economics is scarcity: There is never enough of anything to satisfy all those who want it. The first lesson of politics is to disregard the first lesson of economics.”

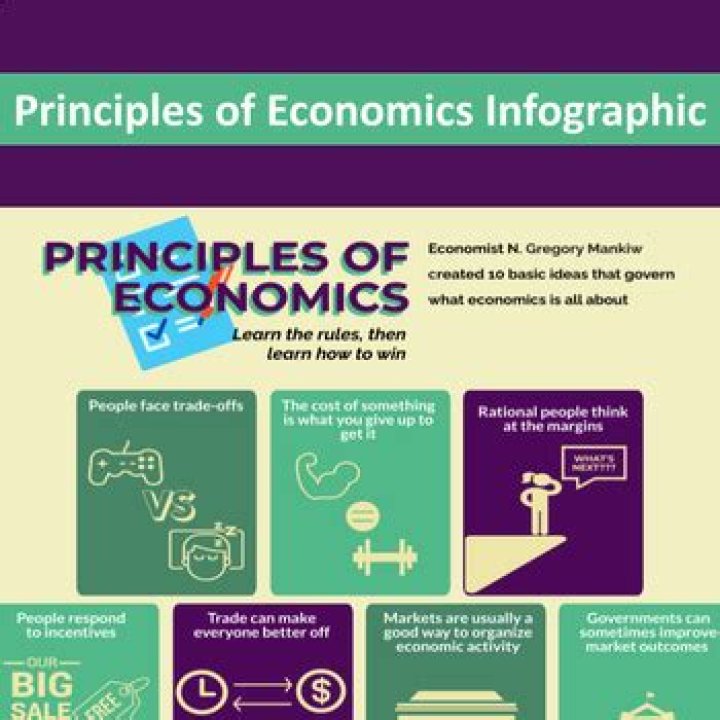

Which is one of the ten principles of Economics?

Mankiw’s status within the economics profession makes him uniquely well placed to help us understand the basic principles of economics. Set out below are Mankiw’s 10 Principles of Economics: 1. People face tradeoffs: To get one thing, you have to give up something else.

What are the principles of Economics according to Mankiw?

the (hereafter unlikely) event of confusion about the basic Principles of Economics. Mankiw’s Principles #1 People face tradeoffs #2 The cost of something is what you give up to get it #3 Rational people think at the margin #4 People respond to incentives #5 Trade can make everyone better off

Who is the author of the principles of Economics?

ECONOMICS is the study of how individuals, firms and government make decisions to manage scarce resources. What does this mean exactly? Professor Greg Mankiw teaches economics at Harvard University and is the author of a popular economics text book called Principles of Economics which is used at many Ivy League schools.

Which is the most important principle of Mankiw?

Before sinking into despair for the fate of the human race, however, the reader would be wise to consider Mankiw’s Principle #4: People respond to incentives. Translation: People aren’t that stupid. The dictionary says that incentive, n., is 1. Something that influences to action; stimulus; encouragement. SYN. see motive.