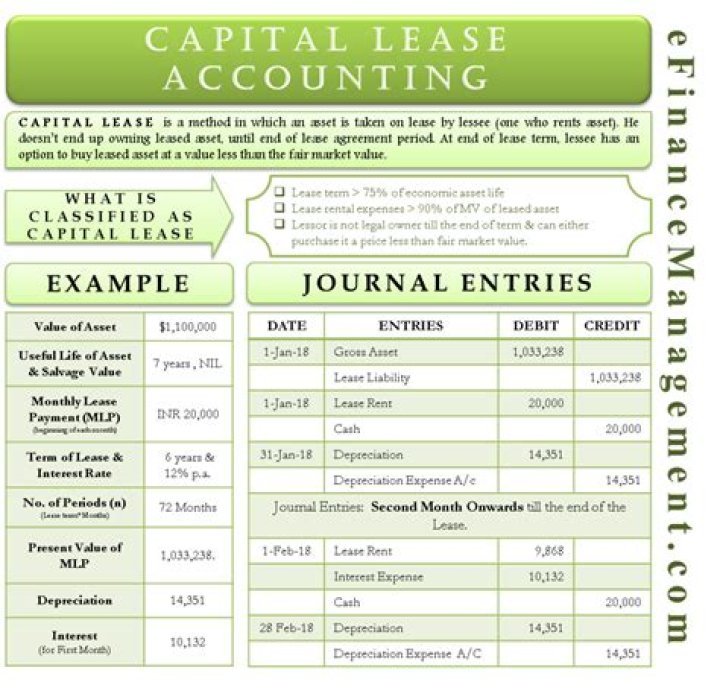

What are leases in accounting?

A lease is an agreement between a property owner and another party who wants to use their asset. There are generally two types of leases which are referred to as operating and financial (or capital) leases.

How do you identify a lease?

At inception of a contract, an entity should assess whether the contract is, or contains, a lease. A contract is, or contains, a lease if the contract gives the right to control the use of an identified asset (‘underlying asset’) for a period of time in exchange for consideration (IFRS 16.9).

How do you account for a lease on a balance sheet?

Reporting the Leases The $1.5 million goes down as a debit to your fixed assets on the balance sheet, and a credit under capital lease liability. Each time you make a payment, you reduce the capital lease liability. You also write off depreciation on the building, just as you would with one you purchased.

What do you mean by lease and how would you classify leases?

A lease is a type of transaction undertaken by a company to have the right to use an asset. Leases generate an interest expense. Interest is found in the income statement, but can also in certain situations. There are two basic categories of lease classification: the operating lease and the capital, or finance, lease.

Is a lease agreement an asset?

Accounting: Lease considered an asset (leased asset) and liability (lease payments). Payments are shown on the balance sheet. Tax: As owner, lessee claims depreciation expense, and interest expense. Risks/benefits: Transferred to the lessee.

Where is lease liability shown on balance sheet?

Finance lease accounting A depreciating asset and an amortizing liability are recognized on the balance sheet. When leasing an asset, it is recognized on the balance sheet at the present value of the future lease payments, usually measured at the company’s incremental borrowing cost.