What are Prepaids in a mortgage closing?

Prepaids are the upfront cash payments you make at closing for certain mortgage expenses before they’re actually due. These include: Homeowners insurance. Mortgage interest. Initial escrow deposit.

What happens to Prepaids after closing?

That payment will include: principal, interest, taxes and insurance. So at closing, they will escrow (or ask you to pay) ten months worth of property taxes so that they have enough to pay a full twelve months when they are due. Same with homeowner’s (or “hazard”) insurance.

Do you have to pay Prepaids at closing?

At closing, you’ll be asked to pay a portion of your taxes and insurance, including private mortgage insurance if applicable, as prepaids for this purpose. “Prepaids are not a closing cost or a fee. They are the borrower’s own funds being put into an escrow account for the purpose of paying taxes and insurance.”

Why do I have to pay Prepaids at closing?

Prepaids are expenses or items that the homebuyer pays at closing before they are technically due. They are necessary to create—pre-fund—an escrow account or to adjust the seller’s existing escrow account. Prepaids can include taxes, hazard insurance, private mortgage insurance, and special assessments.

Who pays Prepaids at closing?

Prepaid items: taxes and insurance Typically, one full year of homeowner’s insurance is collected and prepaid to your insurance company at closing. Alternatively, some homeowners choose to pay this amount prior to closing.

How do you avoid Prepaids at closing?

The most direct way to minimize the cost of prepaid interest is to delay your closing date until the end of the month, but this also means you’ll need to make your first monthly mortgage payment not long after you’ve paid your closing costs.

Do you always get money back at closing?

If you’re buying a house and planning to finance the purchase with the help of a mortgage, the question is bound to come up. The short answer is: You don’t usually get your earnest money back at closing.

Prepaid items are always required at loan closing, whereas escrow accounts are only required in certain cases. Even if you close your loan right before the month’s end, you owe your lender at least a few day’s worth of mortgage interest. This is because your first mortgage payment isn’t due immediately after you close.

Closing costs are fees related to the real estate transaction itself. Included in the closing costs are payments to everyone who has worked on your loan from the underwriter to the appraiser. While many first-time buyers believe the seller is responsible for both the prepaids and closing costs, that isn’t the case.

How are closing costs prepaid in real estate?

Homeowners insurance premium paid up front as well as into an escrow account Real estate property taxes paid into an escrow account Mortgage interest (also known as per diem interest) that accrues between the closing date and month-end Typically, one full year of homeowner’s insurance is collected and prepaid to your insurance company at closing.

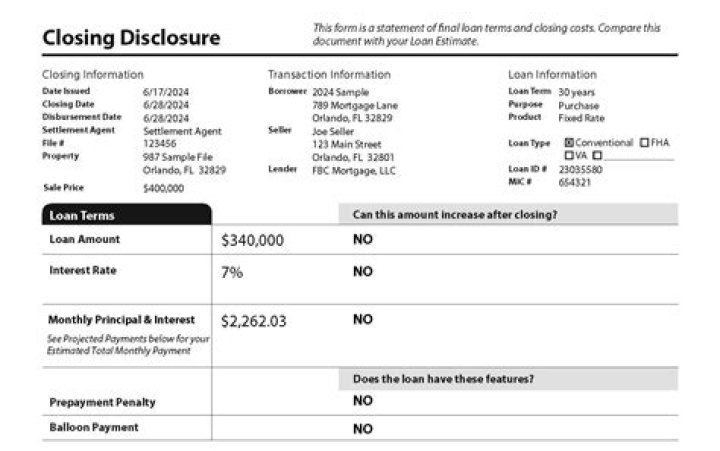

What are prepaid items on a Closing Disclosure?

Prepaid items, listed above, are figures on your Closing Disclosure unrelated to the process of getting a mortgage. The exception to this is upfront mortgage insurance premiums (MIPs) for Federal Housing Administration (FHA) mortgage loans.

Do you pay closing costs when you buy a home?

Although the home seller will sometimes cover closing costs as part of the sale agreement, the buyer always pays the prepaid costs when buying a home. Recall that your prepaid expenses consist of:

What do you need to know about prepaid mortgages?

Here’s what you need to know. What are mortgage prepaids? Prepaids are the upfront cash payments you make at closing for certain mortgage expenses before they’re actually due. These include: These expenses are among the monthly costs of homeownership.