What are some of the key elements of Activity Based Costing?

Five Basic Components of ABC:

- Resources.

- Resource Drivers.

- Activities.

- Activity Cost Drivers, and.

- Cost Objects.

What are the characteristics of ABC analysis?

In materials management, ABC analysis is an inventory categorization technique. ABC analysis divides an inventory into three categories—”A items” with very tight control and accurate records, “B items” with less tightly controlled and good records, and “C items” with the simplest controls possible and minimal records.

Why Activity-Based Costing is needed?

ABC enables effective challenge of operating costs to find better ways of allocating and eliminating overheads. It also enables improved product and customer profitability analysis. It supports performance management techniques such as continuous improvement and scorecards.

What are the 4 steps required for activity-based costing?

Activity-based costing requires accountants to use the following four steps:

- Identify the activities that consume resources and assign costs to those activities.

- Identify the cost drivers associated with each activity.

- Compute a cost rate per cost driver unit.

How do you calculate activity cost?

The formula for activity-based costing is the cost pool total divided by cost driver, which yields the cost driver rate. The cost driver rate is used in activity-based costing to calculate the amount of overhead and indirect costs related to a particular activity.

What are the features of ABC?

The basic feature of ABC is its focus on activities. It uses activities as the basis for determining the costs of products or services. As quoted by Horngren, Foster and Datar, “ABC is not an alternative costing system to job costing or process costing.

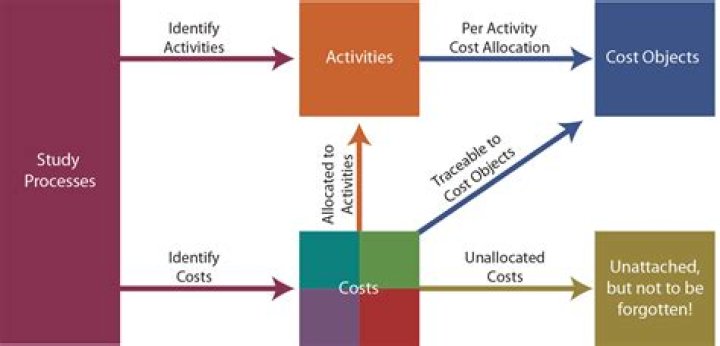

What are the different elements of ABC costing?

They are:

- Identify costs. The first step in ABC is to identify those costs that we want to allocate.

- Load secondary cost pools.

- Load primary cost pools.

- Measure activity drivers.

- Allocate costs in secondary pools to primary pools.

- Charge costs to cost objects.

- Formulate reports.

- Act on the information.

What are essential elements of traditional costing and activity based costing?

Traditional costing adds an average overhead rate to the direct costs of manufacturing products and is best used when the overhead of a company is low compared to the direct costs of production. Activity-based costing identifies all of the specific overhead operations related to the manufacture of each product.

How Activity-Based Costing is used?

Activity-based costing (ABC) is a method of assigning overhead and indirect costs—such as salaries and utilities—to products and services. The cost driver rate, which is the cost pool total divided by cost driver, is used to calculate the amount of overhead and indirect costs related to a particular activity.

What are main features of activities?

Characteristics of Well-designed Activities

- ACTIVE INVOLVEMENT. The more students are actively engaged with their own learning, the more they learn.

- CONFRONTING MISCONCEPTIONS. New ideas and knowledge are largely constructed out of existing ideas.

- MULTIPLE REPRESENTATIONS.

- ITERATION.

- APPROPRIATE USE OF TECHNOLOGY.

How does an activity based costing system work?

A. An activity-based costing (ABC) system first assigns costs to activities and then traces costs from activities to products. ABC assumes that activities consume resources, and products and other cost objects consume activities.

How is an activity classified in product costing?

To classify an activity means to recognize the difference between it and other activities for different purposes. a. For product costing purposes, activities can be classified as primary or secondary. (1) A primary activity is consumed by a final cost object (e.g., a product or customer).

How are direct labour and materials used in activity based costing?

Direct labour and materials are relatively easy to trace directly to products, but it is more difficult to directly allocate indirect costs to products. Where products use common resources differently, some sort of weighting is needed in the cost allocation process. The cost driver is a factor that creates or drives the cost of the activity.

What does ICMAB stand for in activity based costing?

ICMAB ( Institute of Cost & Management Accountants of Bangladesh) defines activity-based costing (ABC) as an accounting method that identifies the activities that a firm performs and then assigns indirect costs to cost objects.